Deloitte Business Club – Power Up Your Investments

13 March 2023

20 March 2023

To solve its current energy challenges and meet its 2050 climate neutrality commitments, Europe plans to significantly increase electricity generation from solar photovoltaic (PV) panels.

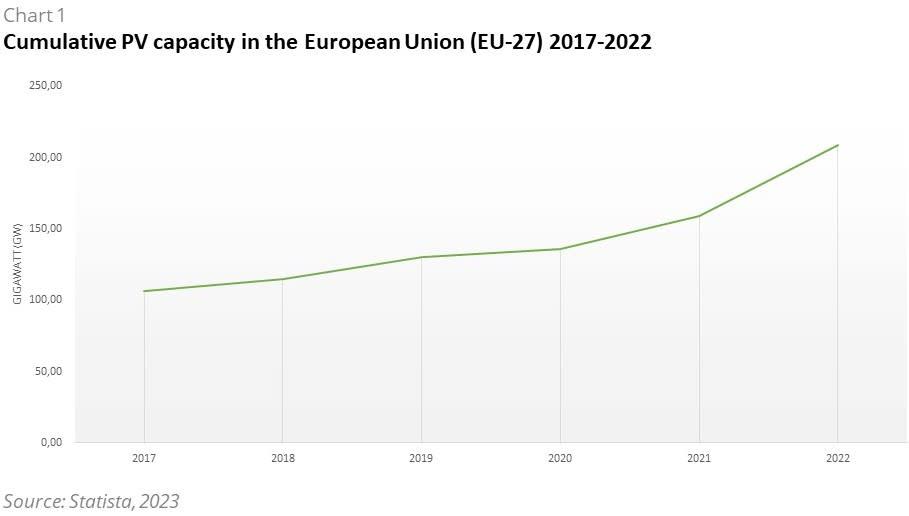

This is part of the "EU Solar Energy Strategy", which has set a target of installing 600 GW of solar PV by 2030, a significant increase from 208 GW in 2022. The increase in solar power generation should help Europe to manage electrification, decarbonise the electricity grid, reduce dependence on other countries and achieve its renewable energy targets while reducing its carbon footprint. Solar photovoltaic (PV) systems are one of the most promising sources of renewable energy and their use is growing rapidly in Europe. However, the production of solar PV systems requires a complex supply chain involving a number of raw materials and components, which are often produced in different countries than the PV modules.

At present, Europe is largely dependent on a single country - China - for the supply of solar photovoltaic panels. It has become the dominant player in global PV panel production capacity over the last decade, overtaking Europe, Japan and the United States. Thanks to investments of more than USD 50 billion in new PV panel supply capacity, China has created ten times more jobs in the solar PV production chain than Europe (300 000 jobs) since 2011. Currently, China's share in all stages of solar panel production, including polysilicon, ingots, wafers, cells and modules, exceeds 80%. While China's significant role in reducing the global cost of PV has many benefits for the clean energy transition, its high level of geographic concentration in global supply chains raises potential issues for governments to address.

In an effort to increase energy independence and reduce carbon emissions, the European Union is actively promoting the local production of photovoltaic systems. At the end of last year, the European Commission officially launched the "Solar Photovoltaic Industry Alliance", which aims to create a European solar PV ecosystem aimed at securing and diversifying the supply of solar PV products. The EU has set a target of producing 30 GW of PV products per year across the entire supply chain by 2025 (it currently has a production capacity of approximately 6 GW of modules and approximately 1 GW of cells and 2 GW of wafers). However, there are several challenges to achieving this goal:

At the same time, the EU and European manufacturers can use several strategies to support and develop their supply chain and PV production:

"The production of photovoltaic panels and the location of the supply chain in Europe is becoming a strategic issue in terms of safety and technological maturity. This opens up space for investors to secure their own projects under relatively favourable conditions of growing demand for PV panels. The question remains, however, how to build their own production and supply chain to be competitive already under existing conditions and possibly redirect some critical raw materials and intermediate products to Europe."

-Miroslav Lopour, Senior manager

Conclusion

Brussels industry representatives stress that the EU PV Alliance is a timely and positive initiative in the light of the current energy and climate crisis and the intensifying global competition for solar cells and modules. An example of the intensifying competition is the US Inflation Reduction Act, which will boost PV module production in the US. To avoid being left behind in this race, the European industry needs financial support to increase production capacity faster. The proposed production capacity of 30 gigawatts would meet around 75% of the annual demand for solar modules in Europe and would also create more than 100,000 manufacturing jobs. Strategies to support and develop the European supply chain and PV panel production could include increasing investment in R&D, promoting circular economy principles, achieving economies of scale and using solar panels to generate renewable electricity on-site.

Deloitte Business Club – Power Up Your Investments

13 March 2023

BP posts record profit in 2022 but lowers its climate targets

10 February 2023

EPH enters the Dutch market

30 January 2023