23 June 2022

Positioning for green: Oil and gas business in a low-carbon world

A spectrum of opportunities for oil and gas companies

As oil and gas companies slowly transition to a low-carbon world, four archetypes emerge—each with distinct metrics for success and value-creation opportunities.

Executive summary

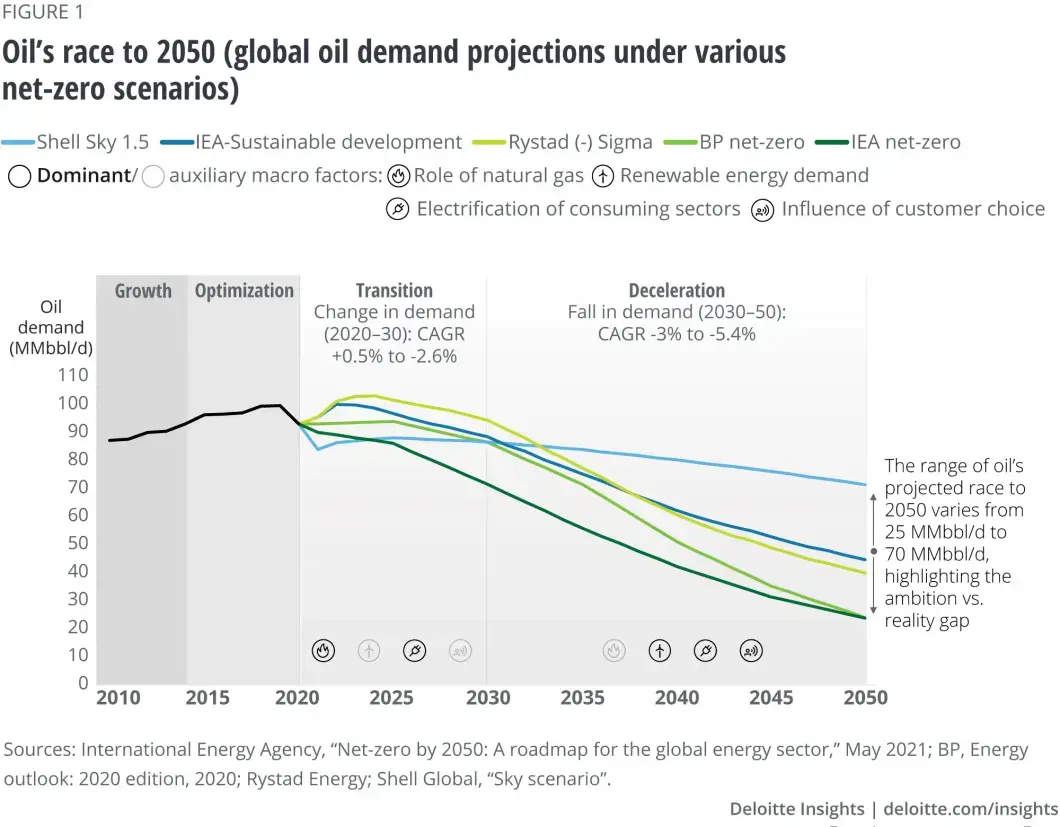

A growing number of oil and gas (O&G) companies are pledging net-zero goals, but not all are clear about how to get there. In a recent Deloitte survey, 56% of respondents view the energy transition as a mixed bag of opportunities, risks, or a complex phenomenon. Successful transition will take a long time, and some prominent energy transition scenarios project oil demand in 2030 to remain around 90 MMbbl/d (figure 1). This implies there’s likely to be sustained value in oil and gas—indeed, an overwhelming 77% of surveyed executives plan to maintain hydrocarbons as their long-term business.

The interplay of energy transition and traditional hydrocarbons creates a spectrum of opportunities, which can be distilled into four archetypes. Net-zero pioneers and green followers are training their sights on renewables and new energy, while low-carbon producers and hydrocarbon stalwarts continue to focus on fossil fuel production. The metrics for success in each archetype are different but are consistent with the steps needed to be a “winner” in that archetype. For example, a net-zero pioneer will be concerned with asset divestments, while a low-carbon producer will focus on decarbonizing field operations. And as a company’s strategy evolves, it may move across these archetypes: A low-carbon producer could move over time to be a green follower. As the market evolves, the role of each archetype will likely be important for the industry to meet both rising energy demand and climate goals.

By associating themselves with an archetype that closely matches their strategy, O&G companies can identify ways to drive value from the transition—and there’s indeed value near US$1.3 trillion to be unlocked. However, companies must address their internal transformation using operations design, supply chain ecosystem, a digital mindset, and organizational setup. Fundamentally, meeting high stakeholder expectations can require each archetype to attain a balance not just between economics and environment, but also between growing the overall market and growing their market share.

Executive survey methodology

Deloitte conducted a survey of 100 C-level senior executives and environment, health, and safety leaders of global oil and gas companies to study organizations’ plans and strategies to navigate the energy transition. It spanned a diverse mix of global upstream portfolios, including integrated companies (68%), domestic pure plays (18%), international exploration and production (E&P; 9%), and national oil companies (5%) with revenues above US$100 million. The comprehensive survey helped uncover the actions that some O&G businesses are taking to address changes in the industry and identify what motivates those businesses to adopt new practices and implement new technologies related to optimizing the hydrocarbons business and/or venturing into clean energy.

The long road to a low-carbon world

The net-zero focus is real and will likely grow stronger by the day. In addition to governments designing policies to incentivize a move to a lower-carbon future, corporate pledges to achieve net-zero goals are pouring in with a growing share of O&G companies joining the race. Irrespective of the time frame—2030, 2040, 2050—these pledges suggest that the global energy system is set to undergo transformational changes. This could mean many things, but most prominently, it signals a reduced role for fossil fuels, higher share of renewables in the energy mix, greater consumer choice, and increasing levels of integration and competition for cleaner technologies.

77% of surveyed executives plan to maintain hydrocarbons as their long-term business, including the 47% who plan to decarbonize the business.

Given the imminent shift, energy agencies, companies, stakeholders, and analysts are increasingly highlighting three broad scenarios: business-as-usual, rapid transition, and eventual net-zero. Although every scenario is a possibility, adopting a business-as-usual mindset and assuming no significant change in societal attitudes toward emissions could risk a company’s survival. And while the argument of those planning for a business-as-usual scenario that green energy isn’t always profitable in the near term holds ground (for more details, read Portfolio transformation in oil and gas), there is no doubt that the energy transition is underway.

However, the energy transition will take a long time to complete. Even by 2050, the most aggressive net-zero scenarios project oil demand to remain between 25 MMbbl/d and 50 MMbbl/d. Also, while recycling could limit feedstock demand growth for plastics in the long term, the overall demand for petrochemical feedstock is likely to remain strong at least in this decade with the increasing use of recycled material in production. Thus, the major deceleration in oil demand will likely start in the next decade. The 2020s is expected to therefore be a period of transition, where many O&G companies will strive to reconcile the reality with the ambition of moving to a lower-carbon energy system.

The other side of the transition

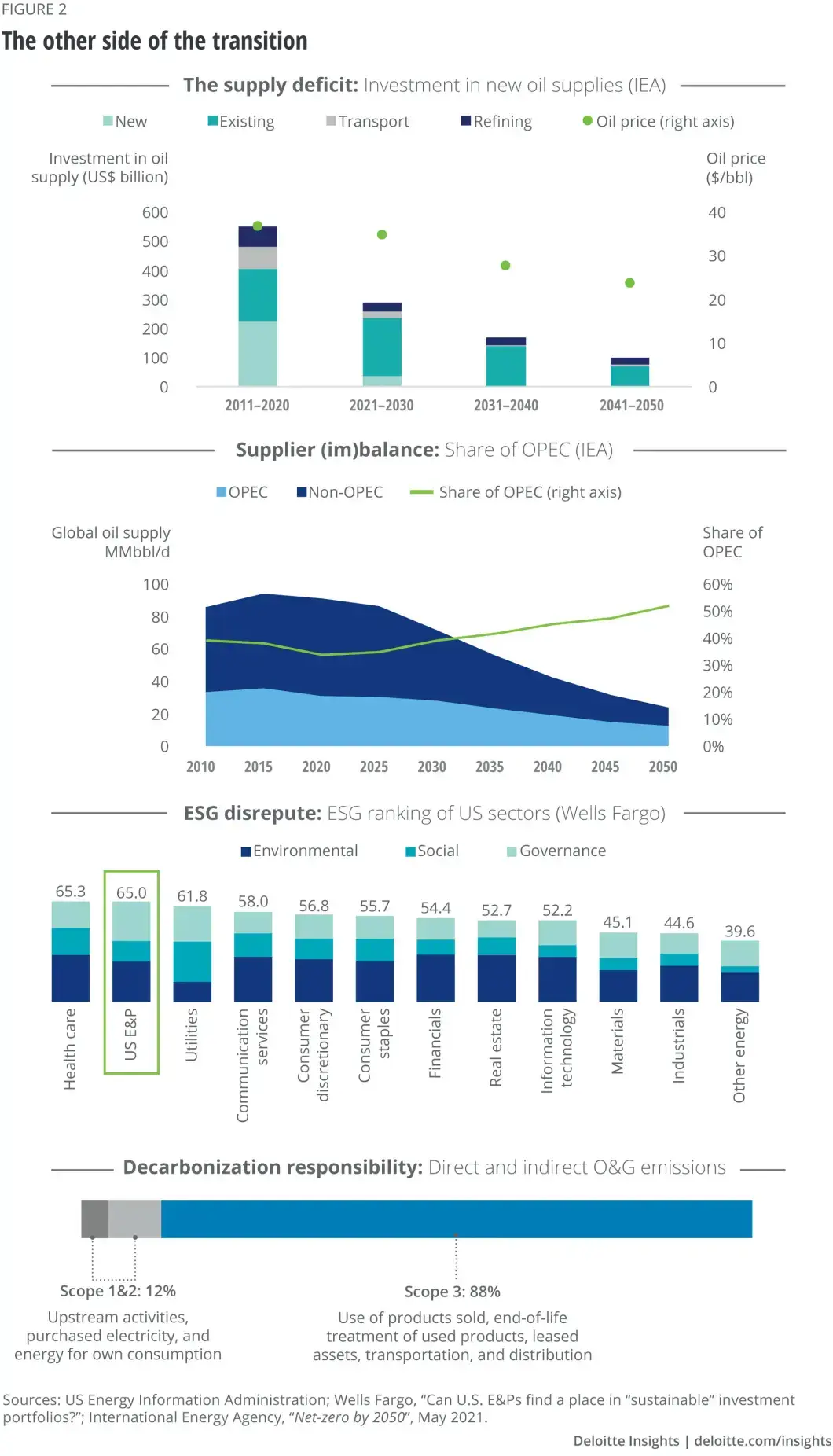

There will likely be a role for oil and gas in the energy mix for years to come due to the law of supply and demand, geopolitics of energy, and the accountability of all companies in the energy value chain in curbing emissions. However, the transition is not that straightforward. Even switching demand for petrochemicals would be challenging without a transition in raw materials requirements of various sectors outside the energy sector. So, what might this new world look like in terms of supply, demand, and pricing fundamentals (figure 2)?

- The supply deficit:Oil supply and demand will likely not move in tandem, at least in this decade. Until recently, demand lagged supply, but a steep drop in capex has changed this equation. Put simply, the green shift won’t necessarily mean low oil prices. Current annual capex is approximately US$375 billion, and minimum annual capex required to offset field declines is estimated at US$525 billion.As a result of the “missing capex,” oil seems to have already come out of its “new normal” price range of US$50-60/bbl.Considering the industry has been optimizing its operations since 2015, a price of US$60/bbl and above would mean added profits for many O&G companies. In this scenario, western O&G companies may even consider going private to get capital from less carbon-sensitive investors and pursue opportunities having higher returns. In other words, the acceleration in energy transition may happen alongside O&G companies capturing high value for their hydrocarbons—at least in this decade.

- Supplier (im)balance:OPEC’s oil market share is projected to increase from 37% currently to over 50% by 2050 under prominent net-zero scenarios, driven in part by international oil companies (IOCs) reducing their O&G capex.If production from nonprivatized producing nations such as Russia is also considered, OPEC+ would be supplying most of the demand by 2050.This could result in a phase where expensive imports from OPEC+ will increasingly fill the demand-supply gap until the world completely electrifies the transportation sector and decarbonizes power generation. And if demand from energy-hungry countries in the Americas and Asia falls slower than expected, and with other unknown sociopolitical factors remaining largely constant, the world may witness significant oil price volatility and energy security risks.

- ESG focus:Environment, social, and governance (ESG) investing is growing, and O&G companies are increasingly focused on not just environmental issues, but also social and governance ones. O&G companies are not outliers in terms of their ESG performance—in fact, many producers have been proactively publishing their ESG performance and setting ESG goals for several years already. US E&P companies, for example, have the second highest ESG scores after the health sector in the United States.Nevertheless, the ability of even top O&G ESG performers to source capital and retain capital is a growing issue.

- Decarbonization responsibility:From court rulings to shareholder activism, the pressure is mounting on O&G companies to reduce emissions and broaden their emission goals, including reporting Scope 3 emissions. Although O&G companies have a responsibility to disclose and reduce Scope 3 emissions, the onus lies across the energy value chain, including industrials and transportation. The O&G industry’s direct emissions (Scope 1 and Scope 2) constitute only 12% of its total GHG emissions.

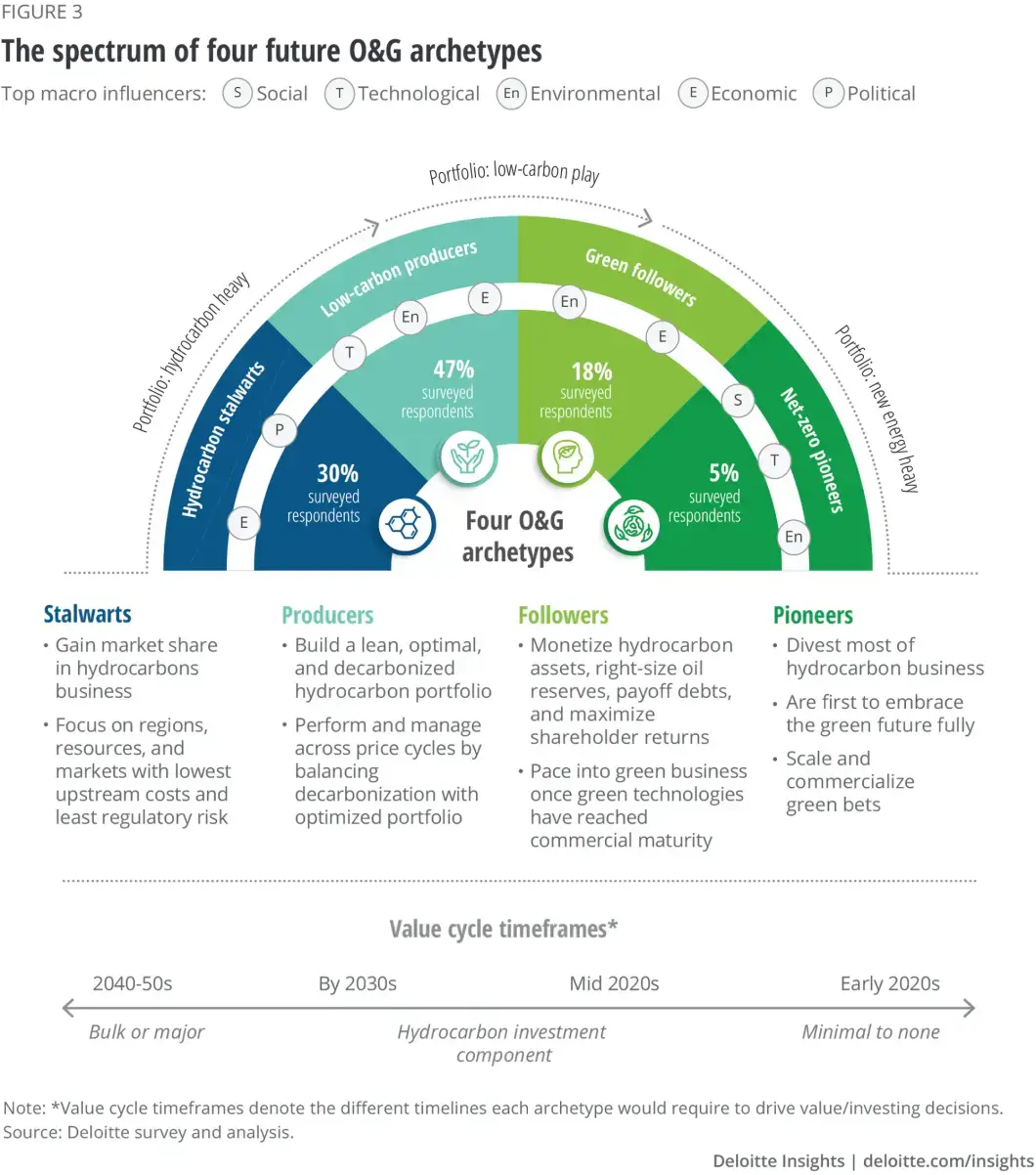

Four archetypes of the future

In a lower-carbon energy system, producers would still be needed to supply the most bearish hydrocarbon demand outlook, while others would play a big role in enabling the successful global energy transition. In our surveys and discussions with O&G companies, four distinct roles—or archetypes—emerge (figure 3):

- Hydrocarbon stalwarts:Those that are primarily focused on gaining market share and nurturing their hydrocarbon business in regions/assets with the lowest upstream costs and least regulatory risk

- Low-carbon producers:Those that are primarily focused on building a lean, optimal, and decarbonized hydrocarbon portfolio

- Green followers:Those that enter the new energy business after hydrocarbon assets are monetized and clean technologies have reached commercial maturity

- Net-zero pioneers:Those that are focused on building a primarily new energy heavy portfolio by divesting most of their hydrocarbon business and are the first to embrace the green future fully

Below, we examine the potential opportunity across the four archetypes.

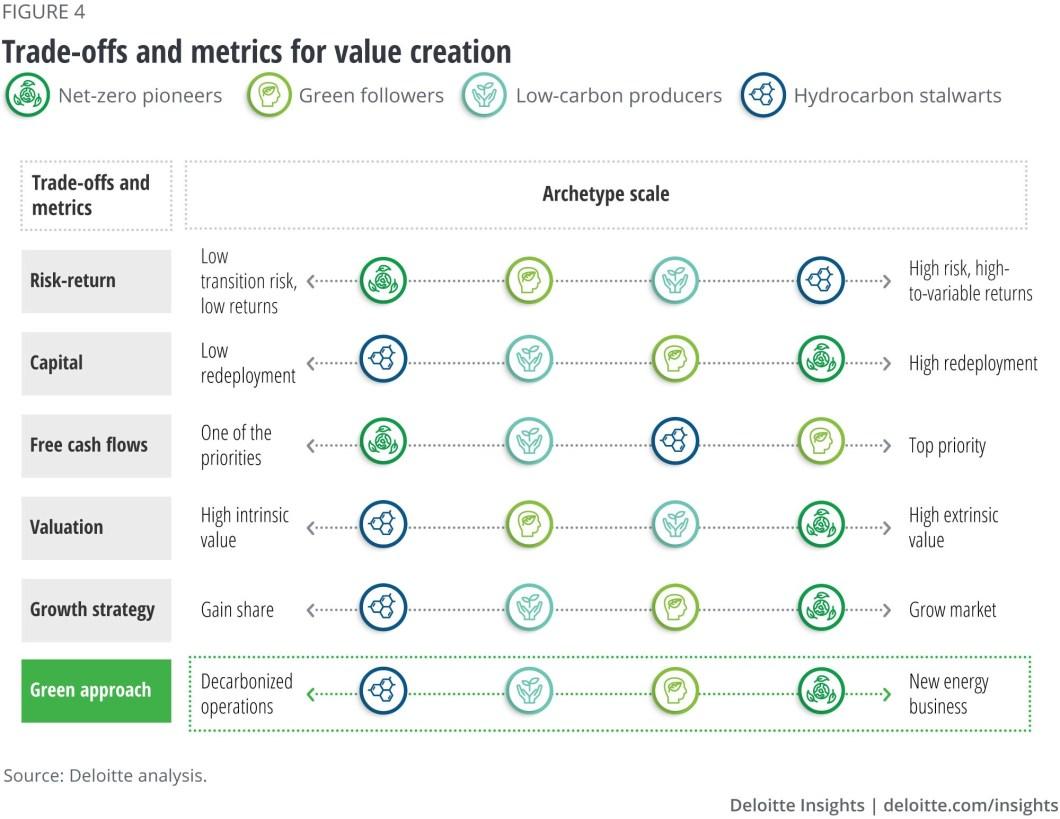

A game of trade-offs and choices

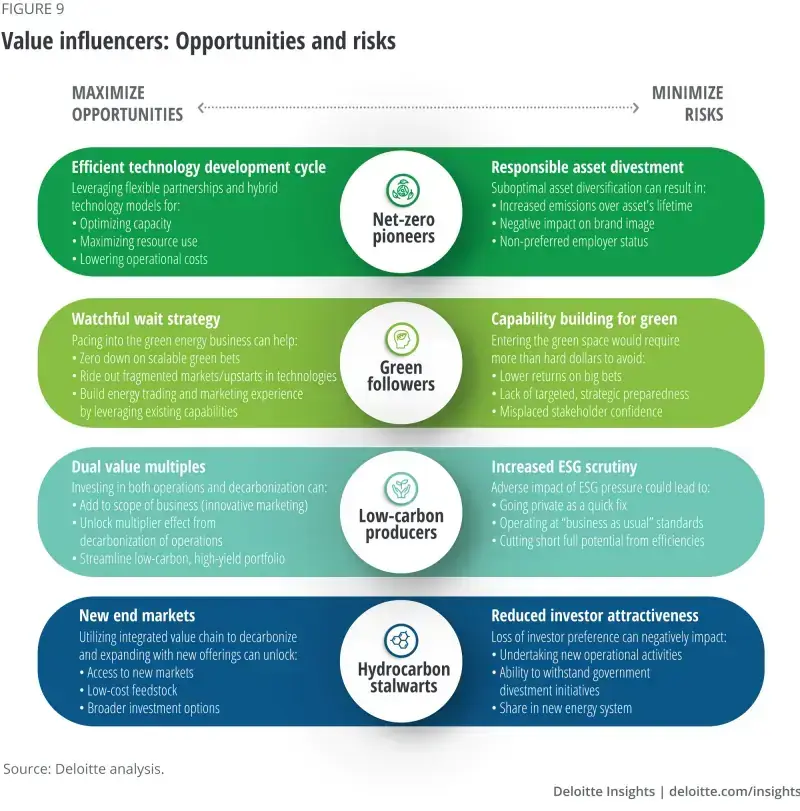

As O&G companies plan for the future, they face several complex decisions that will define their view of value generation and success. Prioritizing between capital and cash flow targets, risk-return trade-offs, scope of valuations, and growth will create the distinctive “recipe for success” for each archetype (figure 4). While net-zero pioneers would favor minimizing the transition risk, stalwarts would likely play the high-risk high-return game, at least in this decade. Similarly, while green followers and net-zero pioneers target high extrinsic valuations, low-carbon producers and hydrocarbon stalwarts will likely bank on their strong intrinsic valuations. Irrespective of the choices made by each archetype, going green (ESG performance, decarbonized operations, or new energy) is a non-negotiable metric enabling or disabling the rest. On the other hand, doing it right could unlock a “green” multiplier impact across the spectrum, which brings the archetypes closer together, with some even intersecting and overlapping in the future.

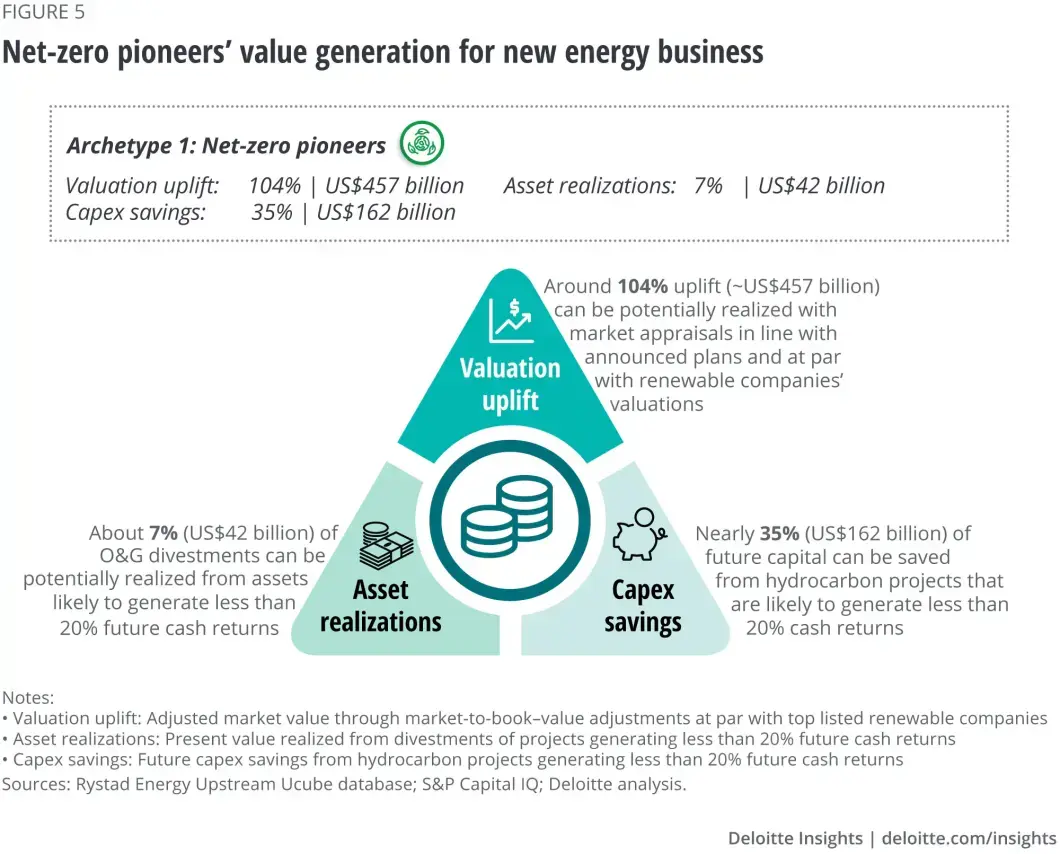

Archetype 1: Net-zero pioneers

Net-zero pioneers have a bold vision of making sustainability their core business, the courage to dismantle or divest their hydrocarbon business model built over decades, and the patience to scale and commercialize their green business. These three green traits are hard to embrace, especially at an oil price of US$75/bbl—which is probably why only 5% of surveyed O&G executives associate with this archetype or pathway currently. Nevertheless, there seems to be growing internal activism for going green.

According to our analysis, some of the largest integrated O&G companies have announced net-zero targets and a departure from hydrocarbons as the primary business feature under this archetype. While relatively fewer in number, they still account for 30% of the industry’s market capitalization—that is, they have the power to move the needle for their regions and industry.

Despite their bold moves, these pioneers seem to receive less market or stakeholder appraisals—especially as compared to, for instance, companies identifying as “renewable utilities,” which have surpassed several supermajors in terms of market capitalization and are receiving three times the valuations attracted by today’s net-zero pioneers. Other factors aside, even receiving valuation multiples at par with these companies would mean an upside of 104% (i.e., US$457 billion) in shareholders’ wealth for these handful of net-zero pioneers (figure 5). Similarly, if pioneers identify hydrocarbon portfolios generating less than 20% in cash returns, they could consider redeploying about 35% of planned capex (US$162 billion) and potentially divest ~7% to realize value of about US$42 billion.

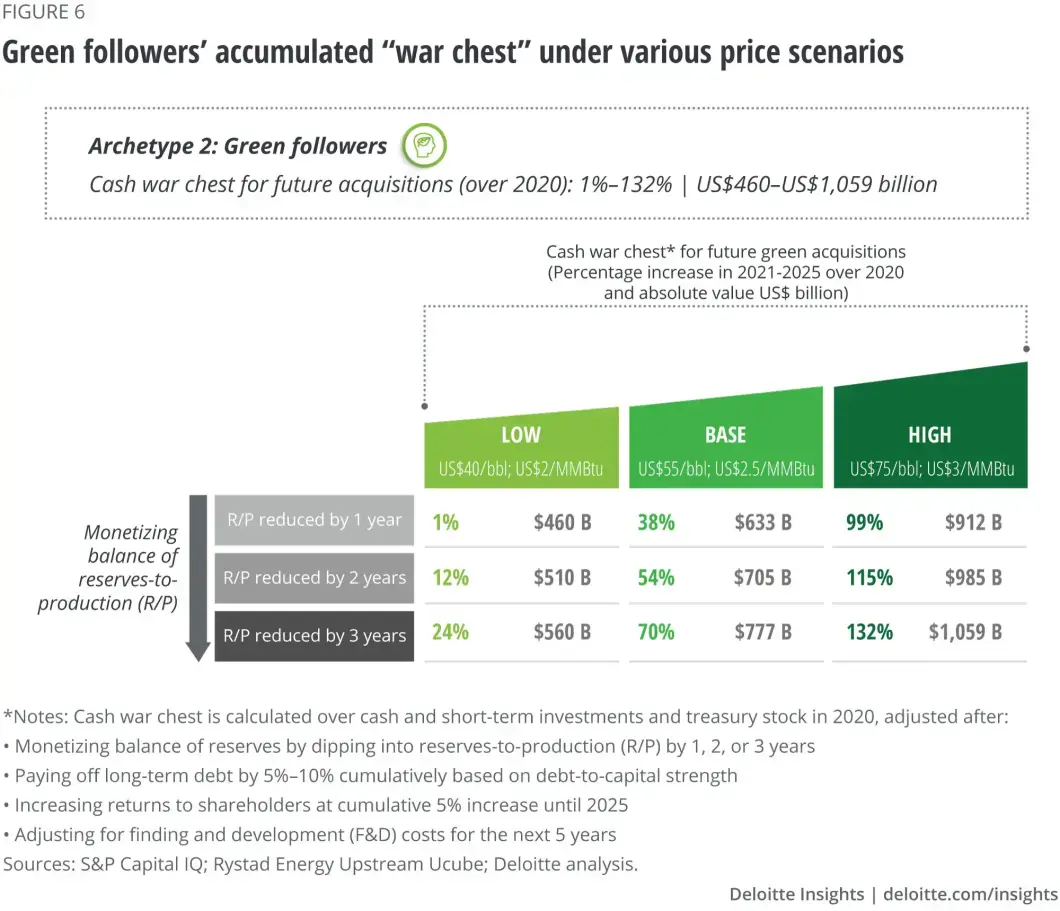

Archetype 2: Green followers

With oil prices trading above US$75/bbl, staying in hydrocarbons, rectifying balance sheets, and managing shareholder expectations look attractive to some companies. They will develop a war chest to acquire green businesses once the economics and technological evolution make sense. According to our survey, 18% of O&G executives expressed that this strategy aligns most with their long-term strategy.

Although going green would be an eventual goal, it may not have the first claim on the followers’ extra cash generated—that is reserved for reducing debt and increasing payouts. Additionally, companies may start slashing and monetizing their traditionally higher reserves-to-production (R/P) that could now be less relevant for long-term business growth (see sidebar, “The reserves-to-production equation”). Would this leave enough for the green business? According to our analysis of probable green followers, there is an opportunity to build a war chest of about US$705 billion—i.e., 54% over and above the cash held in 2020—after reducing R/P by two years at an oil price of US$55/bbl, slashing long-term debt by 5% to 10%, and increasing shareholder payouts by 5% until 2025 (figure 6).

The reserves-to-production equation

The industry’s age-old metric to judge its direction and pace of growth—the reserves-to-production (R/P) ratio—highlights the number of years for existing reserves to run dry at current production levels. In the past, a drop in R/P used to be a result of major disruptions—and was punished by investors.

With uncertainty looming over oil demand, investors are placing less value on holding reserves on balance sheets and companies are rethinking high R/P. Also, oil prices influence the value of reserves, i.e., low prices can push the balance into red as companies can technically no longer produce them economically.

The opportunity to monetize the excess reserve base and battle the challenge of long-term demand uncertainty would be timely in this decade as demand and prices both stay resilient.

Is this war chest sizeable? Probably yes. It is 1.5 times the cumulative market capitalization of all publicly listed renewable energy companies in the world. Additionally, the wait may allow them to buy big at lower valuations, as green technologies evolve and mature over the next few years.

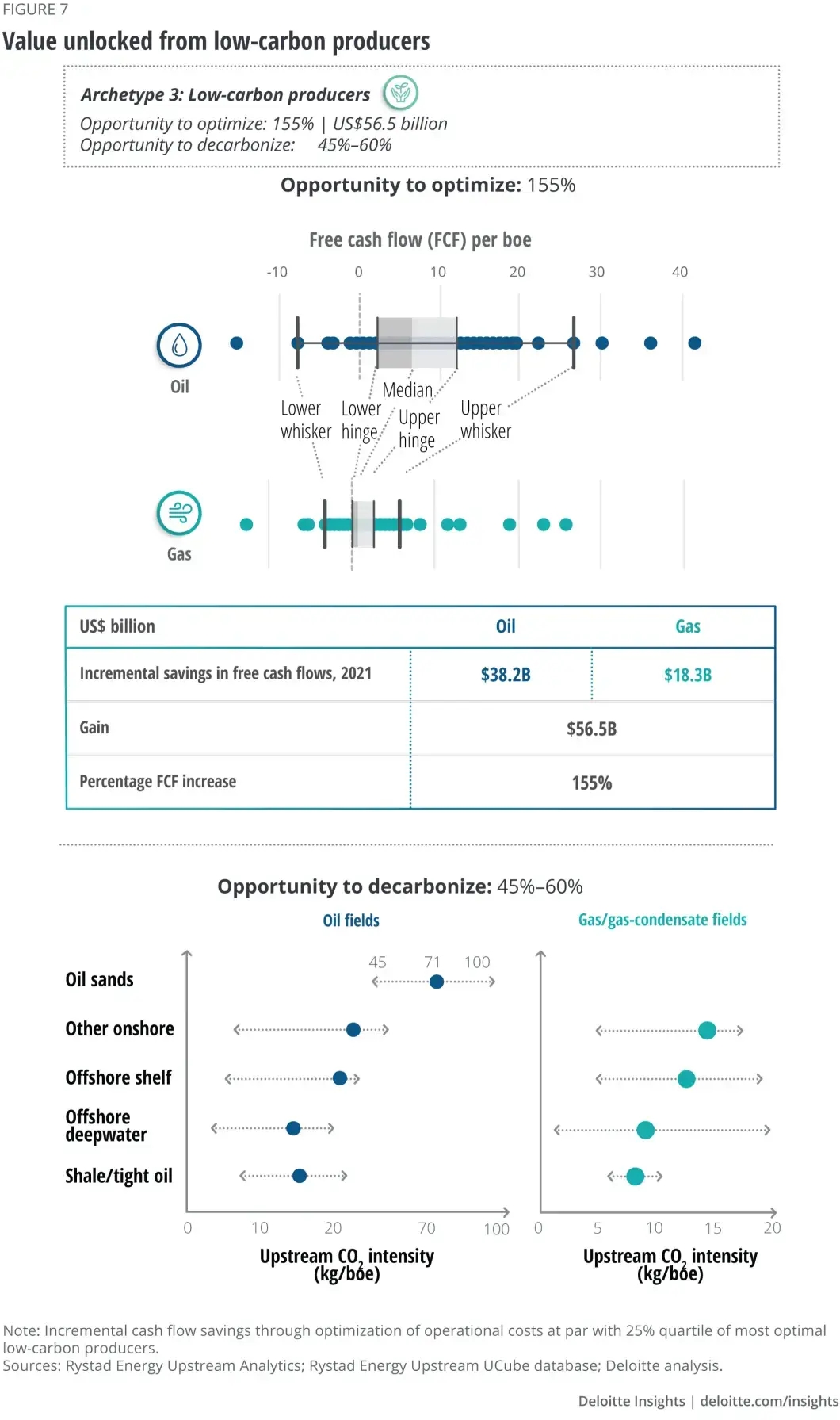

Archetype 3: Low-carbon producers

In the past decade, many O&G companies have made a sea change to their fuel, regional, or resource strategy, led by the availability of new supply, changes in demand centers, and the new normal of oil prices. However, lean producers with the lowest carbon and most efficient portfolios have weathered and navigated every downcycle successfully. These producers will likely continue to have a role in the new future of energy, especially those that strive for both optimization and decarbonization. According to our survey, 47% of O&G executives stated that the pathway of low-carbon producers aligns most with their company’s long-term vision.

While low-carbon producers have already adjusted the most to the new oil reality, there is significant scope to further optimize their operations—for instance, through their well engineering and completion designs (figure 7). If they follow, for example, the best practices of the top 25% optimizers within this group, they can increase their annual free cash flow by as much as US$56.5 billion or 155%. Just for comparison, the highest free cash flow of the group has been US$49 billion until now.

Meanwhile, the opportunity to decarbonize is sizeable for this group. The decarbonization potential largely depends on the type of reserves and hydrocarbons produced but implementing industrywide best practices could reduce emissions intensity by up to 45%-60%. The low-carbon producers would likely try to offset their hydrocarbon emissions by improving their operational efficiency and focusing on using their existing assets for carbon storage as well as enhanced oil recovery (EOR) projects. For instance, US independents could possibly gain value in this space as it will help them not only offset their emissions from their onshore shale assets but also drive increased revenue.

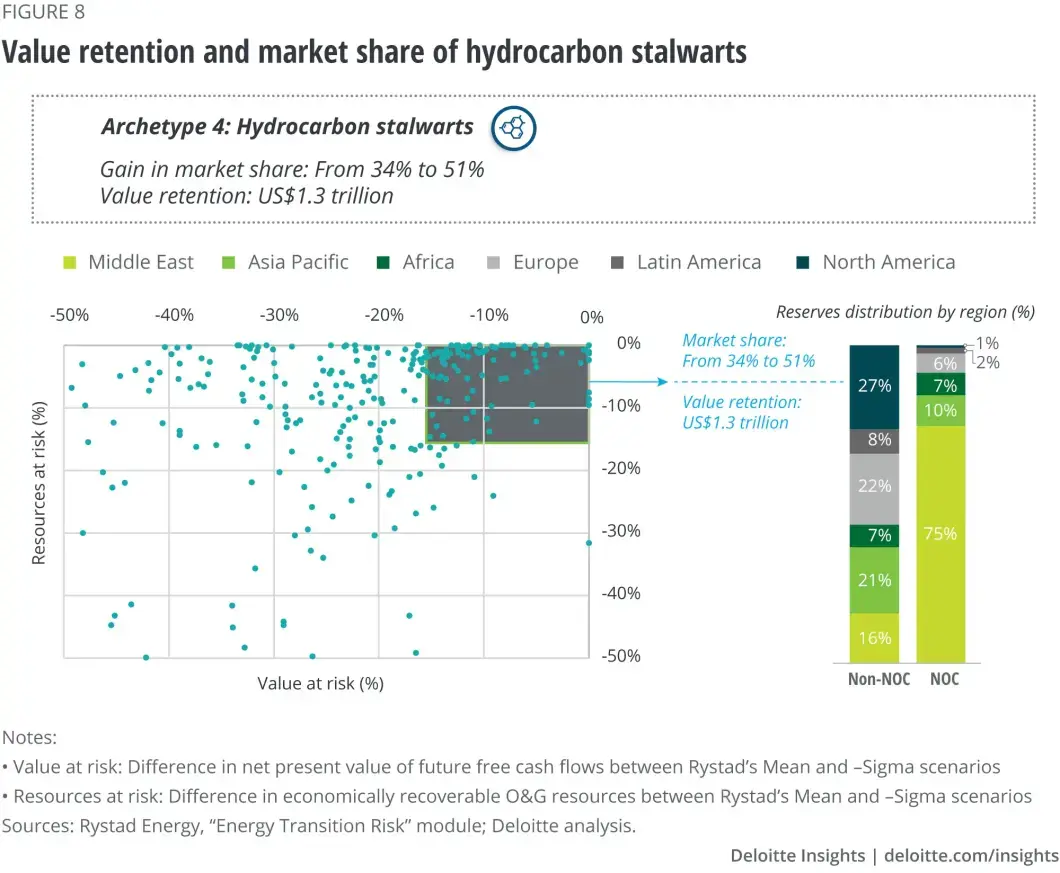

Archetype 4: Hydrocarbon stalwarts

Hydrocarbons are synonymous with many oil-producing nations where the national oil company (NOC) plays a large role in the country’s economy. By holding the most competitive reserves and benefitting from operating the biggest fields, many producing countries (or their NOCs) tend to have a natural advantage in growing their share in oil’s projected decline. In fact, a few of these nations or their NOCs also offer a combination of competitive reserves and decarbonized operations. For instance, Saudi Aramco flares less than one-fourth of the natural gas flared by all US upstream operators put together, despite production of both falling within close range of each other.

Stalwarts have the potential to gain market share by as much as 34% today to 51%. However, it is not that only NOCs will be the “last supplier standing.” Many publicly or privately owned companies, in fact, have lower hydrocarbon “value and resources at risk” than many NOCs. For instance, of the companies that have less than 16% of their hydrocarbon portfolio “at risk” from a decline in cash flows and recoverable reserves, 57% are non-NOCs (figure 8). Many of these non-NOCs have built strong positions in regions with the least transition risk, lowest cost structure, or certain demand base. Almost 50% of the reserves held by them are in conventional onshore basins, which offer the lowest decline rates among all the resource types.

By associating themselves with an archetype that closely matches their strategy, O&G companies can identify ways to drive value from the transition- and there's indeed value up to or near trillion dollars for each to be unlocked.

With 30% of O&G executives stating that the pathway of hydrocarbon stalwart aligns most with their long-term strategy, it seems that many O&G companies still see value in a smaller hydrocarbon market. Stalwarts with less than 16% of their hydrocarbon portfolio at risk, in fact, may reap US$1.3 trillion of value by 2050, if overall oil demand lands halfway between 25 MMbbl/d (net-zero) and 50 MMbbl/d (accelerated transition).

Net-zero pioneers

Going green can help pioneers overcome multiple challenges, including negative image, capital constraints, trickling flow of incoming talent, and improved access to low-cost finance. In fact, funding costs of low-carbon O&G debt issuers in North America are 75 basis points lower than that for carbon-intensive borrowers with an additional six years on the bond tenor, providing greater capital raising flexibility.

As the novelty of going green matures, low-carbon technologies evolve faster-than-expected, and keen competition emerges among the commercially viable ones, pioneers could be judged and differentiated on how well they can make good on early green bets. Rightly so, about 80% of surveyed senior O&G executives that identify as net-zero pioneers highlight technology evolution as their topmost challenge. They need to be alert to opportunity and agile in pursuing it, while balancing gains and risks by adopting flexible partnerships and hybrid technology models or empowering low-carbon ventures.

Further, divesting the pioneers’ hydrocarbon assets in an improved price environment would be favorable but could give rise to a dilemma as buyers with poor carbon profiles emerge. Selling assets to such buyers may result in a net-addition, not net-zero, to the environment and would lead to negative reactions from stakeholders, investors, and even regulators, as noticed when a major oil company divested assets to Scotland’s largest carbon emitter or in another case, to a closely held, “almost invisible” operator. Sellers need to live up to their social obligation of responsible divestment, where they don’t make an asset’s lifetime emissions a buyer’s problem and simply move on.

Green followers

A watchful wait strategy can help green followers gradually build the future “green” capital required, ride out the nascent green experimentation phase, and maximize hydrocarbon value at higher prices. They can also zero in on scalable economical bets, which aren’t fragmented and crowded with upstarts, as currently seen in the solar PV and onshore wind space. These technologies are seeing 95% of global annual capacity additions, with internal rate of return (IRR) hovering around 6%–7% for solar PV and 9%–10% for onshore wind (as against many oil projects delivering more than 15% IRR at US$50/bbl).

Capturing the above band of IRRs or picking a more competitive new energy solution altogether would require much more than hard dollars from green followers. Leveraging existing hydrocarbon infrastructure for new energy solutions (e.g., offshore wind), establishing a new corporate structure to commercialize low-carbon technology portfolios, building an extensive energy trading and marketing experience, identifying corporate PPA opportunities, and entering into strategic partnerships especially on the transportation and storage front of green energy (aka new midstream) could be some starting points for green followers. For instance, Quidnet Energy and Emissions Reduction Alberta (ERA) partnered to develop an ultra-low-cost form of hydroelectric energy storage, using technical O&G expertise of well-drilling and high-pressure pumping to store renewable energy in shale formations.

Right messaging and a clearly communicated strategy, maximizing or maintaining shareholder returns, and engaging with M&A advisers and strategists early on can effectively help build out these opportunities. Timing the cycle may not be the only point—timing companies’ readiness is important as well.

Low-carbon producers

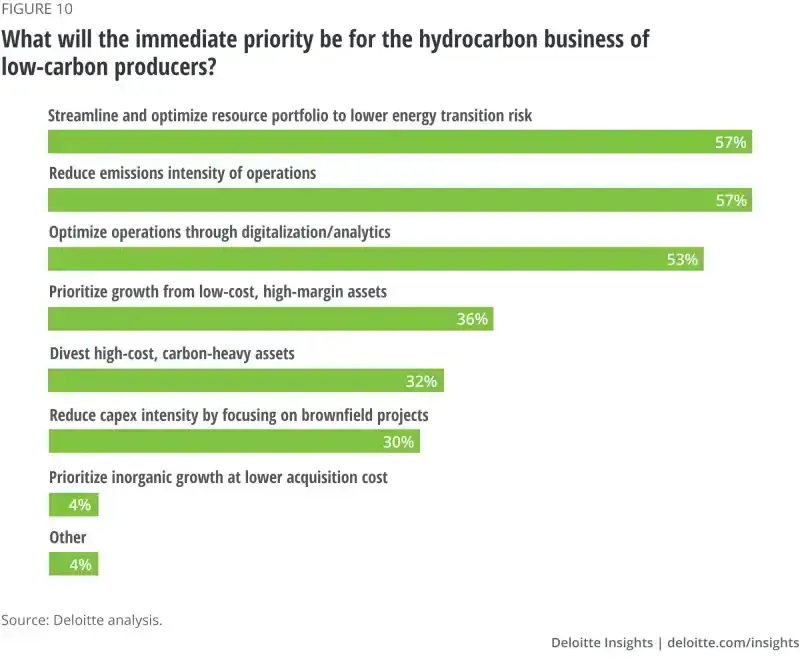

Low-carbon producers have to balance economics (operational efficiency) and environment (decarbonization) to be a lean machine from day one and create a domino effect in the long term. Any investments they make in automation, energy efficiency, advanced leak detection, quantification technology, etc. serve this dual purpose. In fact, about 55% of surveyed producers’ immediate priorities for their hydrocarbon business are to reduce the emissions intensity of operations, streamline resource portfolio to lower the energy transition risk, and optimize operations through digitalization/analytics (figure 10). For instance, a major international E&P is defining its operational performance as a function of both, lower cost of production and lower emissions intensity, and has been trading ahead of analysts’ net asset valuations due to its combination of low-cost, low-emitting, and higher-yield assets.

Going forward, companies should bring more than just an engineering efficiency mindset to develop their business and grow innovatively. There is big value, for instance, in shaking up the status quo to become innovative marketers. Lundin recently made headlines for its sale of the world’s first certified carbon-neutral oil from its Edvard Grieg field, which has five times less CO2 per barrel of oil than the world average. The company aims to achieve full carbon neutrality of all its production by 2025.

The way forward is to keep doing more—in other words, using stakeholder pressure to achieve best-in-class results (operationally or ESG-driven). Metrics of project evaluation, performance assessment, and reporting transparency have to evolve and go beyond “this is how we operate.” Producers that balance all three—portfolio, business optimization, and emissions—can truly unlock value on this path.

Hydrocarbon stalwarts

Hydrocarbon stalwarts, especially Middle East and North African (MENA) and Russian NOCs, have a built-in advantage or a head start in the net-zero race: They own the large reserves that can be developed and produced comparatively cheaply.34 Additionally, their position to be the “last one standing” will likely be supported by net-zero pioneers’ and green followers’ early shift away from oil and gas. Playing just for the market share, however, shouldn’t be the strategy of the stalwarts. Similarly, having a small portion of their portfolio consisting of natural gas and owning a simple integrated value chain won’t maximize gains or minimize risks for them.

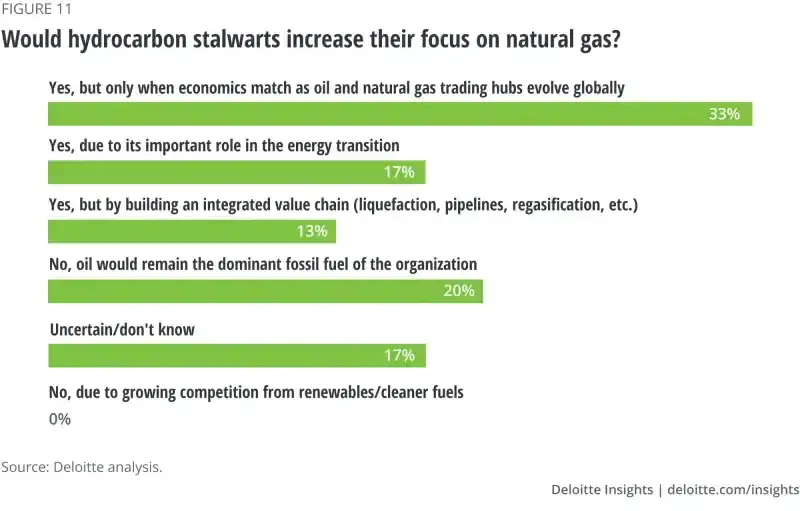

About 60% of the long-termers plan to increase their focus on natural gas, dependent on a few conditions: when its economics match that of oil, natural gas trading hubs evolve globally, gas utilities transform, and they have a commercial and financial capability to own positions across the natural gas value chain (figure 11). Similarly, only those stalwarts who look at integration as a means to buoy demand for their hydrocarbons and create new revenue streams—as against simply securing a market for their crude oil—will likely thrive in the unfolding transition. Companies could also look for integration within petrochemicals to broaden access to end markets. Additionally, the integration would be more meaningful if it allows them to cut and control Scope 2 and Scope 3 emissions, an area where IOCs or pure-play independents can struggle due to their limited control over the entire value chain.

Saudi Aramco, for example, plans to spend US$110 billion on the biggest shale gas development in the Jafurah gas field (Saudi Arabia) to produce green hydrogen rather than LNG. Similarly, both Saudi Aramco and ADNOC are leveraging their expertise along with their existing midstream and downstream infrastructure to become major blue hydrogen and ammonia exporters. In the long term, however, even MENA-based NOCs under this group could face capital constraints, as competition emerges from pure-play green companies. Thus, stalwarts that are focused on corporate governance, efficiency, and innovation could be best placed to tackle the challenges and thrive.

Turning the lens inward

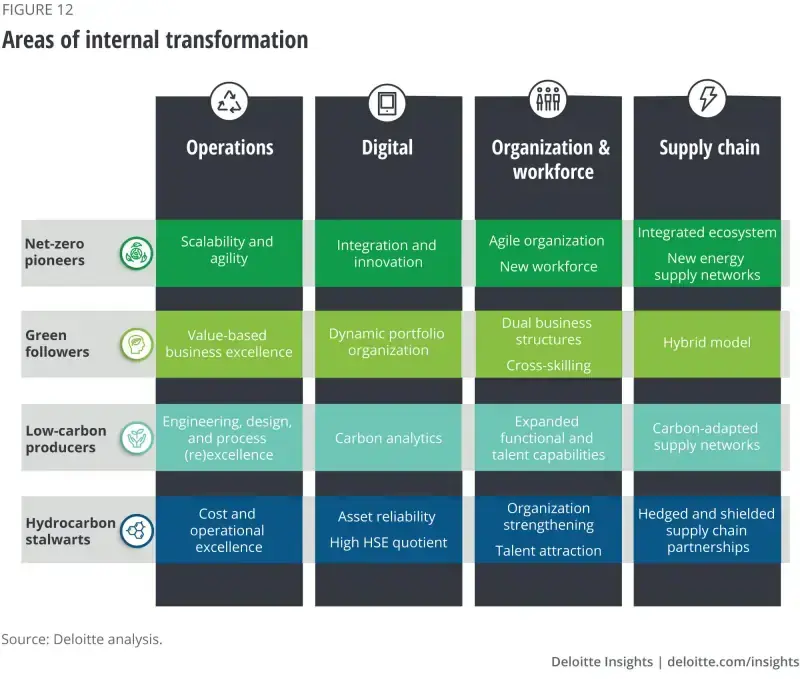

The value and success of each archetype will be determined by how well each initiates its internal transformation. Progress on four capabilities—operations design, supply chain ecosystem, the digital mindset, and organizational setup, including workforce planning for tomorrow—would differentiate the rate of value creation across the archetypes (figure 12).

Operations

While the industry has always prioritized operations optimization, the challenge is intensifying with the transition. For example, low-carbon producers and hydrocarbon stalwarts could possibly struggle to operate fields and plants at peak capacity due to falling demand. But there are ways to unlock value across the archetypes.

Net-zero pioneers can nurture operational agility and synergies to develop new technologies and services at lower costs. Meanwhile, green followers can drive operational synergies across their existing hydrocarbon and new green asset base. Offshore operators, for example, can significantly reduce their capital intensity, considering 40% of the full lifetime costs of a standard offshore wind project overlaps with an offshore O&G project.

Low-carbon producers can shift their operational focus from developing hydrocarbons to capturing carbon. This would involve retrofitting existing assets and redesigning processes to reduce the carbon footprint while extending asset life. For example, Phillips 66’s reconfiguration of its San Francisco refinery to produce renewable fuels is expected to reduce the facility’s greenhouse gas (GHG) emissions by 50%, while ensuring continued asset use despite shifting product slate. Hydrocarbon stalwarts, on the other hand, can focus on cost and operational excellence to become the lowest cost producers, thereby ensuring profits despite oil price volatility.

Digitalization

Digitalization holds different priorities for each archetype as stalwarts and producers pursue optimized and decarbonized operations given stringent regulations, while pioneers and followers seek any competitive edge while entering new markets.

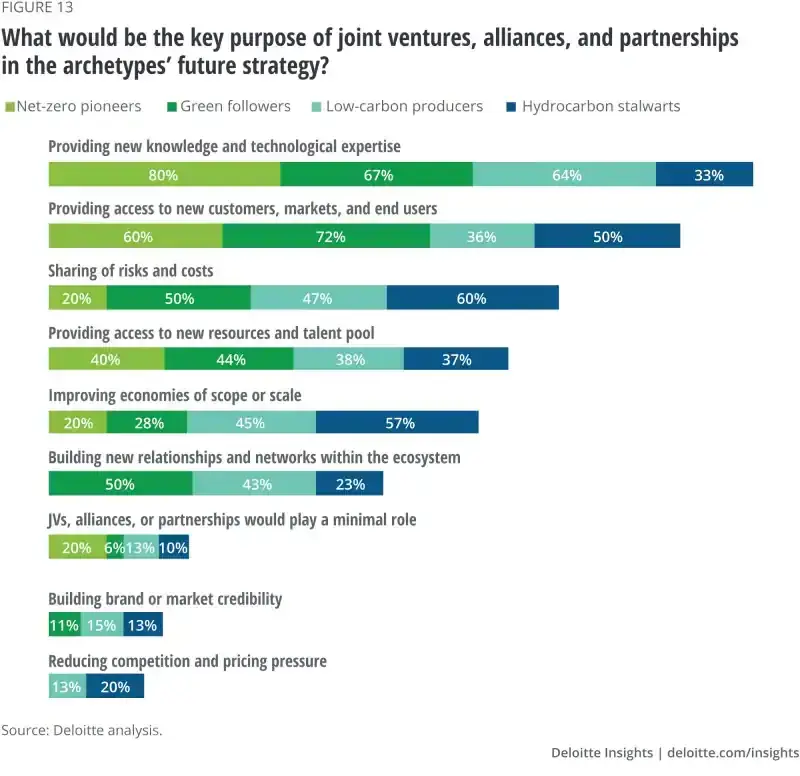

Net-zero pioneers can integrate existing digital networks and systems while adding or innovating new technologies. This would help scale operations quickly, track data in real time, and identify capabilities for a fast-evolving digital workforce. Meanwhile, green followers can develop data-driven models powered by next-generation technologies such as predictive intelligence and advanced analytics to be in sync with the shifting energy demand. Switching the portfolio also requires new technological expertise and robust digital infrastructure which, according to 56% of our survey respondents, can be enabled through joint ventures, alliances, and partnerships (figure 13).

Low-carbon producers could benefit from edge-based analytics and blockchain solutions translating operational data into measurable carbon metrics to improve brand image, governance standards, and visibility across the carbon value chain. Repsol is leveraging blockchain to optimize the certification process for its petrochemical plant, likely to result in operational savings of about half a million dollars annually. Hydrocarbon stalwarts can focus on asset reliability and improved worker safety by leveraging technologies, such as augmented reality and virtual reality to develop and train operators without any inherent ESG risks.

Organizational and workforce transformation

Net-zero pioneers may have to be agile operators to compete for talent with startups and corporations venturing into renewable energy. Their organizational structure should represent their distinct shaping business priorities, witnessed in the case of a wind energy operator that recently revamped its corporate structure into separate functional divisions catering to different customer segments. Green followers could have to build two corporate structures/cultures for driving value and cost optimization in hydrocarbons, while building new capabilities in renewables. Harmonizing the two structures and upskilling/cross-skilling talent should be the priority of green followers’ management.

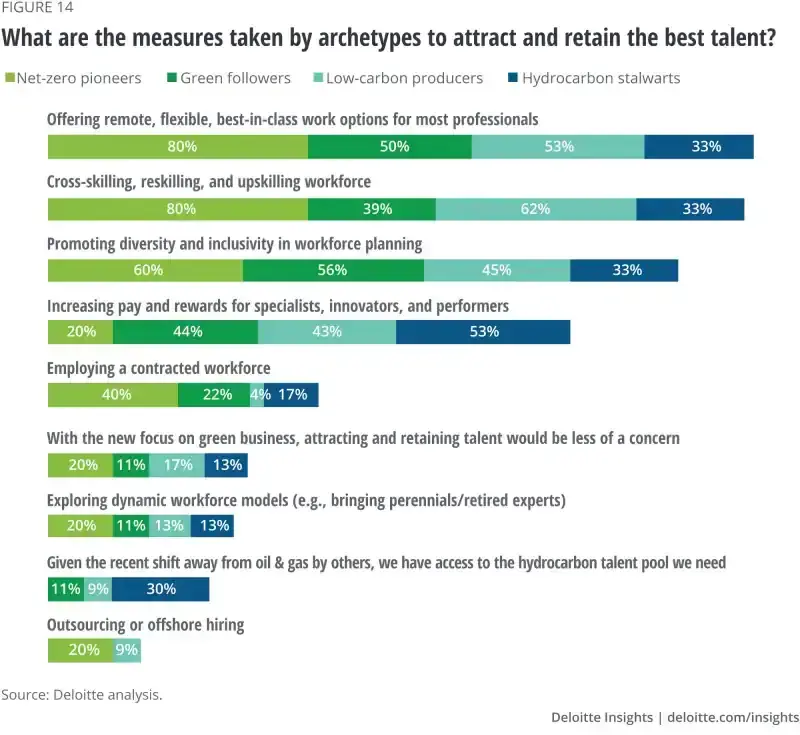

Low-carbon producers could have to redefine mandates for hydrocarbon experts to reduce emissions from the fields and resources under management. This could put the spotlight on new roles for energy and carbon analysts to deliver enterprise-level carbon assessments, monitor carbon calculations and progress, and recommend changes to internal processes. Although 30% hydrocarbon stalwarts expect to have sufficient access to the expert hydrocarbon talent pool as other companies shift away from the business, flexible work options, higher pay, and promoting diversity and health could help attract and retain talent, apart from strengthening the organizational setup (figure 14).

Supply chain

Evaluating the risk profile of each supplier and visualizing risks at each node of a supply chain has become a bare minimum in a post–COVID-19 world. Net-zero pioneers face an elevated challenge of establishing a new supply chain and integrating a concentrated set of OEM suppliers, for products such as ammonia and hydrogen. Addressing this challenge would require them to scale up their partnerships and build an integrated energy supply network. Meanwhile, green followers should consider a multistakeholder hybrid supply chain model that reduces costs, drives innovation, offers scalability and, most importantly, provides an emission-abating solution to all.

Low-carbon producers, especially those involved in aggregating or exporting hydrocarbons, could benefit from undertaking an audit of emissions across their supply chain as their customers are expected to increasingly demand information about life cycle emissions of their purchased commodities. For instance, Cheniere Energy is working toward measuring and reporting emissions on its exported LNG cargo from 2022 to educate customers on their carbon footprint and to offset life cycle emissions using carbon credits. On the other hand, hydrocarbon stalwarts—especially MENA NOCs that are dominant suppliers and have more control over their supply chain—may hedge and shield their supply chain vendors from oil price shocks and provide support to upgrade their systems. Saudi Aramco, for instance, is working with banks and financial technology companies to launch a type of corporate cashing program called supply chain finance to support the cash flows of its vendors.

Fueling the future together

The low-carbon future will likely be characterized by a smaller oil market, which would be a more competitive one. For the companies who continue to focus on hydrocarbon production, lean operations, and low production costs are expected to provide a competitive edge. And companies who exit the oil markets to focus on new low-carbon business models will need to differentiate themselves in these new areas. As soon as the industry masters the balance of economics and environment, it can smoothly win in the third “e”—the energy market of the future. In doing this, the O&G marketplace is likely to undergo a complete transformation, from portfolios and partnerships to platforms and innovation.

The four archetypes will need to evolve to make sustainability their core business. For instance, a hydrocarbon stalwart with the lowest-cost operations also can decarbonize O&G operations and even unlock existing infrastructure to build new revenue streams (e.g., blue hydrogen and ammonia). Who moves when and how fast will determine the value unlocked by each.

Although timelines may differ, participating in the transition to the low-carbon future can unlock a multiplier effect and establish a new equation for companies across the spectrum. Companies that balance their internal transformation and corporate vision, leave room for innovation and agility, and set a strong “low-carbon” foundation, are likely on the right path.

The four archetypes will need to evolve to make sustainability their core business. Who moves when and how fast will determine the value unlocked by each.