Merger between Smurfit Kappa and WestRock

14 September 2023

3 October 2023

The first activity that private equity firms encounter when entering the market is fundraising, i.e. finding and raising funds from external sources. This is a key step in the entire business model, as it determines not only its subsequent scale, but also whether it takes place at all. But what does the fundraising process entail in practice, who is involved and how long does it take? We have summarised this and other information for you in our article.

Whether you are aware of it or not, many of the services you can utilize for yourself or your business are provided by firms with private equity backing. Private equity is constantly present in our daily lives, whether it be while purchasing lottery tickets from Sazka, learning English online with Blabu, or keeping a digital journal with Vos. Are you using Memsource's translation tools for your business? PE-backed. Using Resistant AI to protect your AI system from cyberattacks? PE-backed.

What, though, is private equity? What does it mean to "fundraise"? Who is involved in the fundraising process? This article deconstructs the fundamentals of fundraising in PE funds, a key idea for anyone interested in learning about—or working in—a sector tangential to—the private markets.

One definition of private equity distinguishes venture capital from private equity (a European concept), whereas the other categorizes venture capital as a subclass of private equity (an American concept). However, the goal of both concepts is to acquire a business to increase the value of the asset over a predetermined period of time and eventually sell the company to a different buyer.

In other words, private equity is an asset type that provides equity capital to businesses resulting in minoritarian, majoritarian, or whole ownership in the investee business. These businesses represent a broad spectrum of industries from different parts of the world and in various stages of growth.

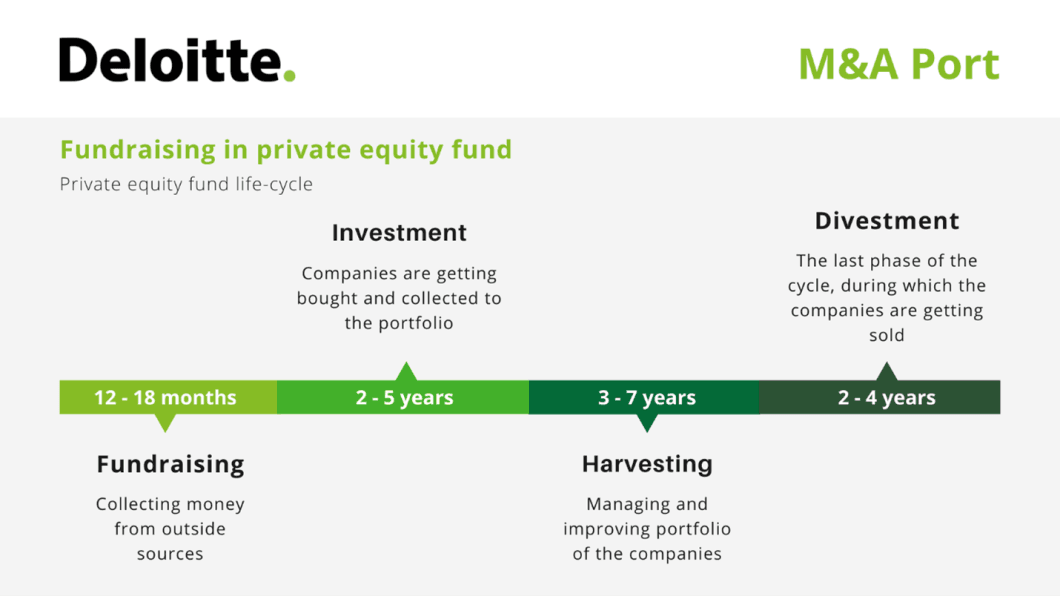

The phases of a private equity firm's business model are as follows:

The first phase of the PE fund life cycle is the fundraising. It is a procedure through which a PE company launches a private equity fund and obtains money from investors. Fundraising, in more precise terms, is the process through which the PE firm pitches its business plan to potential investors. The authorized fund manager contacts potential investors to express the PE fund's goals through a presentation or a private placement memorandum (PPM). These offering documents should include clear strategy (e.g. industrial and geographical focus), terms, policies, processes, and control mechanisms of the PE fund. Additionally, the limited partnership agreement is written to address the fund structure from a legal and tax standpoint, as stipulated in agreements.

Fundraising's fundamental goal is to raise money over a 12- to 18-month period to establish the fund. Since closed-end PE funds are typical, investors may only decide to commit money at the start of the PE life cycle. It is impossible to make further investments after the fund has been closed or withdraw money from it before its expiration date. Before committing their wealth to the fund for an extended period of time, investors in this situation may depend exclusively on the fund managers' established reputations, suggested business plans, and other factors.

Fundraising has different stages, that are called closings. Once a sufficient amount of funding has been secured, and investor commitments have been made, the first closing will begin. Following the fund's start, its operations and first investment prospects are formally assessed. However, the marketing keeps looking for further investors until there is enough investor interest and the present cap is reached. The final closing takes place approximately 6 to 18 months following the initial closure.

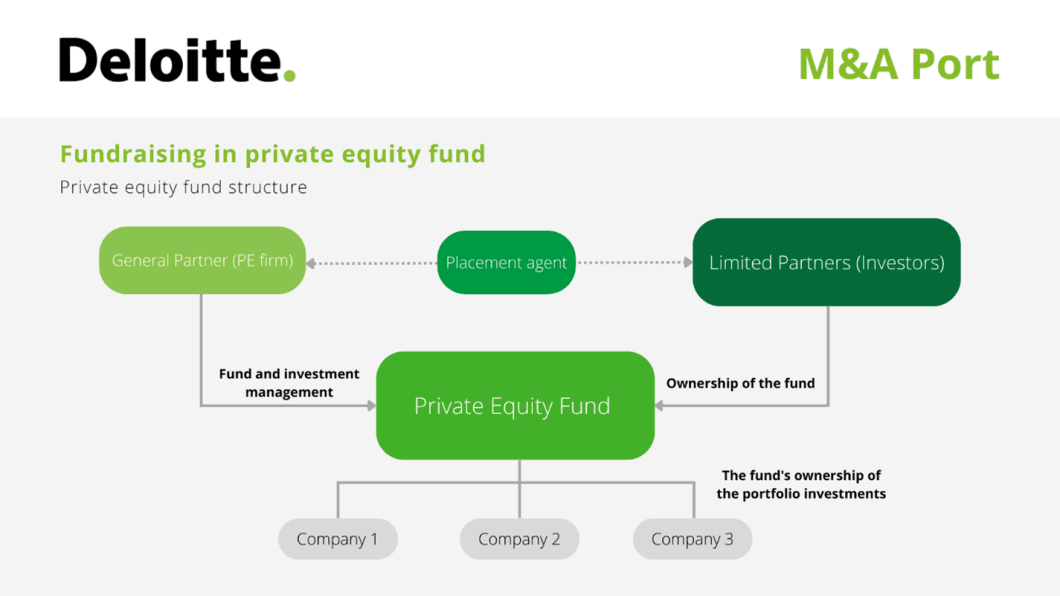

The ability to raise money is crucial for the later phases since it determines the fund managers' abilities to invest and, more crucially, their deal-closing skills. Since it involves more than just money-raising—namely, the development of connections between the fund managers and investors—fundraising is a crucial step in the life cycle of a PE fund. When it comes to connecting investors and entrepreneurs, the PE firm acts as an intermediary. By contributing their skills and knowledge in discovering and evaluating new enterprises, private equity firms decrease the information asymmetry between investors and entrepreneurs. It enables investors to participate in initiatives that uninformed outsiders might reject. Three parties are involved: the GP (General Partner), the LP (Limited Partner), and the placement agent.

General partners may have a challenging time entering the PE market if they have never managed a fund before. As investors rely on their prior results (track record), GP finds it difficult to convince LP to provide funds. In such case, GPs often tends to hire a placement agent to help them connect with investors and present them with their competitive advantage with new insights. In case LP decides to commit their capital to the fund and if the fundraising was successful, these agents are generously compensated by a negotiated fee based on the amount raised.

General partners raise funds from Limited partners, screen investment opportunities, identify and select target companies and also GPs are involved in the company on the operational level. General partners play an active role in the whole process. In contrast, limited partners are passive and do not participate in managing the portfolio companies or the private equity firm itself.

Although the primary source of capital comes from LP, GP obtains a disproportionate share of profit once investments are made. On one side, this aligns with GP's total exposure and unlimited liability for investments. On the other, LP's are liable up to the amount they have committed.

General partners should be highly specialized with solid competencies within the industry. Prior to any acquisition, the investment team vets an opportunity and creates a strategy for the target company to maximize its value. PE firms have a discipline guiding them in every step of their decision ranging from proceeding with an investment to walking away from an opportunity if a red flag (possible deal breaker) is uncovered. There is a large set of crucial skills that these individuals need to possess. The highly skilled general partner will be responsible for:

Limited partners are capital-committing investors. An LP commits a certain amount of money, known as committed capital, to a fund during the the fund's existence. The GP typically makes all investment decisions; hence the LP typically has no right to vote on those decisions. An LP Board is occasionally used by funds to review offers before making final investment choices. The GP updates the LP on the success of the fund's investments throughout the year via quarterly or semi-annual reporting packages. Annual LP meetings are also held at funds.

There are several different types of LPs:

Another person who may be involved in the PE process is a placement agent. This person plays a crucial role as the mediator in the fundraising phase, during which helps PE funds raise money. A placement agency might be as big as a massive division of a multinational investment bank or as small as a one-person independent enterprise. Private equity funds employ placement agents to help them rapidly and effectively acquire capital by connecting the fund managers with eligible investors. The expertise of a placement agent is essential for attracting large potential investors and quickly and effectively running the whole process of fundraising.

PE funds can acquire the target with pure equity (cash deal at signing) but would aim to refinance as much of the equity invested as possible (60-70%) through bank financing. Although, the banks would usually lend an amount not exceeding the targets Net Debt/EBITDA of 4.0x. Moreover, the PE funds would try to combine senior, as well as junior finance to maximize the amount of debt placed on targets balance sheet.

PE funds’ performance appears to be difficult to assess and compare due to their illiquidity and long-term nature. Although, there is one indicator, that can measure how successful the investment was. Internal Rate of Return (IRR) indicates a compound return of a series of cash flown over the investment period. In this case, time is really matter while calculating it. IRR is based on the concept of time value of money; this means the shorter time period, the higher IRR. Moreover, there are two types of IRR:

Other tool, which is also may evaluate the fund’s performance is money multiples. This indicator is easier to calculate, because it does not reflect time value of money, this widely used in practice. Although, there is one big disadvantage – until the last divestment, only meantime performance can be tracked, thus fluctuation over the life of a fund happens. There are several types of money multiples:

Merger between Smurfit Kappa and WestRock

14 September 2023

The third biggest transaction in Czech M&A history

29 November 2022

Exchange membership changes

24 November 2022

Suspension and exclusion of the issue of IAA FQI IFPZK

16 November 2022

Changing the name of the issue NORTONLIFELOCK

9 November 2022