Deloitte M&A Index 2024 Q1

28 February 2024

28 March 2024

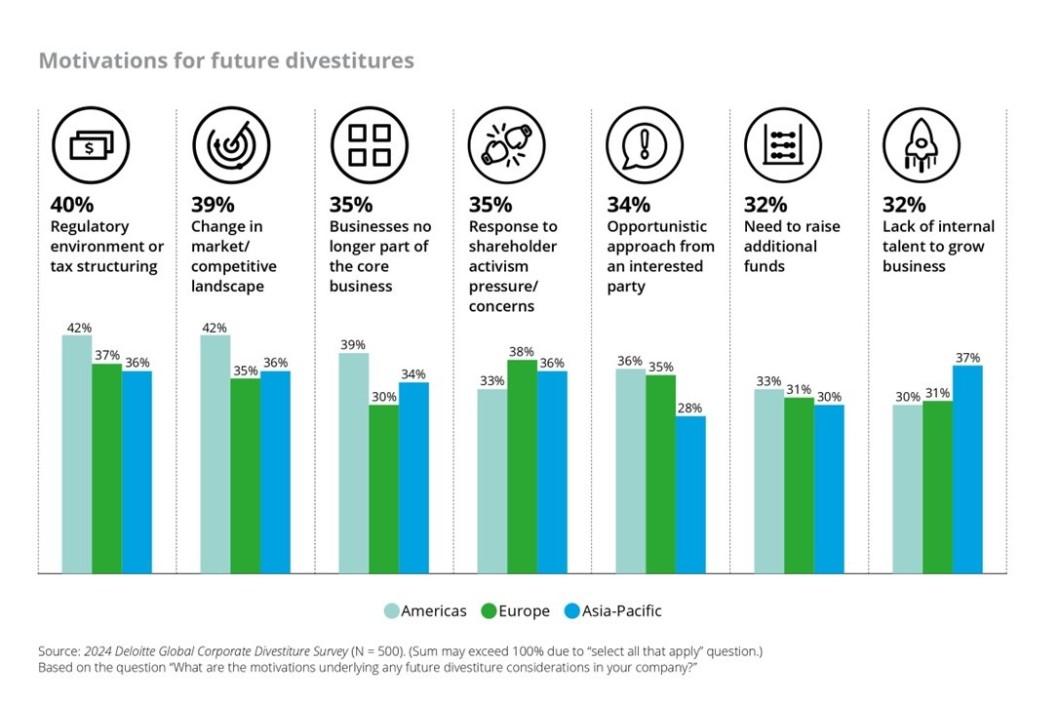

In our latest Global Corporate Divestiture Survey of mergers and acquisitions (M&A) and restructuring leaders, we explore not only the latest trends in divestiture, but also its changing role in corporate strategy.

Except for a pandemic-related spike in 2021, where total global divestiture value topped US$1 trillion, the volume and value of divestitures and spinoffs has remained largely stable in recent history. The outlier year, 2021, found many organizations divesting non-core assets to free up cash after the pandemic slowed and shuttered so much business activity. The next year, 2022, brought just as rapid a cool-off to pre-pandemic levels, in part because ready buyers had been accommodated, and in 2023, volume and value declined even further.

With the most significant market disruption seemingly behind us, are organizations focussing on divestiture-readiness for 2024 and beyond? The latest market data suggests that there is a positive outlook for renewed M&A activity, including divestitures, as this survey indicated that dealmaking is likely to rebound, with fewer than 2 percent of respondents saying their organizations plan no sell-side activity, and almost 80% anticipate three or more divestitures in the next year and a half. It is likely that sellers remember the heightened activity of 2021 and have an appetite to make divestitures a more regular part of their plans.

Read the full report here: 2024 Global Divestiture Survey | Deloitte

Deloitte M&A Index 2024 Q1

28 February 2024

EQT raises €22 billion for latest PE fund

27 February 2024

Capital One to buy Discover for $35 billion

21 February 2024

A new edition of the M&A index is being prepared

16 February 2024

Private Equity Confidence Survey Central Europe 2024

9 February 2024

M&A: How was 2023 and what will 2024 bring?

4 January 2024

Deloitte is the top financial advisor in CEE

1 December 2023

PE fund KKR to buy the rest of Global Atlantic

30 November 2023

Financial Advisory Digital Family

27 November 2023