EQT raises €22 billion for latest PE fund

27 February 2024

28 February 2024

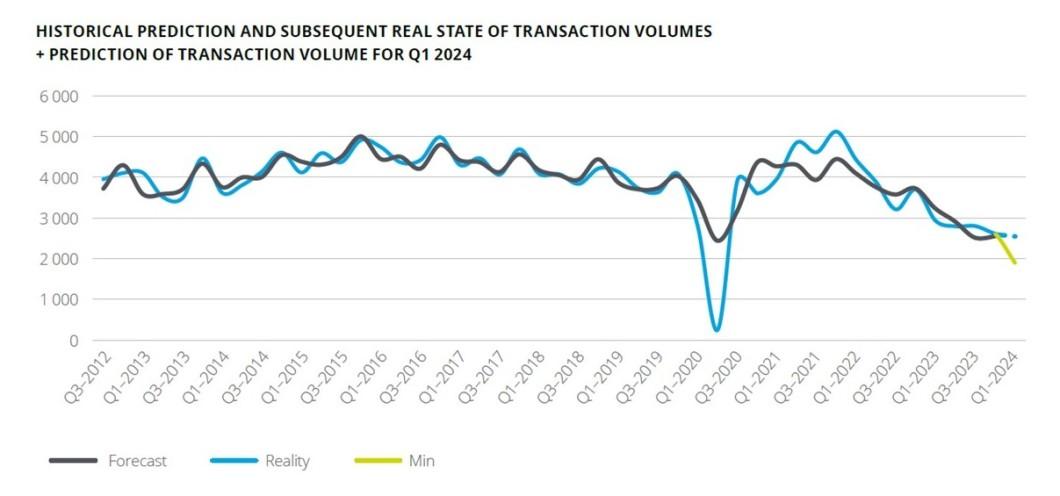

Given the relatively stable number of deals in the previous two quarters and a slightly improving economic environment, the Deloitte M&A Index for the current quarter expects only a slight decline in the number of deals. The forecast expects 2,506 deals, a similar number to the previous quarter, while the pessimistic forecast projects 1,905 deals.

"If the pessimistic scenario were to come true, we would expect a drop to 1,905 transactions. However, such a possibility would only come into play in the context of significant market turbulence, with both Germany and the UK falling into a deeper recession and uncertainty about the pace of interest rate cuts. These circumstances could then impede a rapid recovery and potentially cause a more pronounced market downturn. However, despite the possible drop in the number of transactions in the current quarter, there is still reason for optimism, supported by expectations of lower interest rates and a continued economic recovery. Active portfolio management, including strategic acquisitions and divestitures, remains key for companies operating in a volatile market environment," says Miroslav Linhart, Managing Partner, Financial Advisory Services, Deloitte Czech Republic

The M&A markets continue to be supported by cash balances of unallocated private equity capital, which at the end of last year held a value of approximately USD 2.49 trillion. Both financial and strategic investors are expected to re-enter the market at an accelerated pace this year and - buoyed by the surprisingly strong health of the banking sector - continue to seek investments in high-quality assets, such as companies with strong market positions, long histories or workable business strategies.

"Cash reserves and unallocated private equity capital continue to bolster M&A markets, with investors poised to capitalize on strategic acquisitions. As economic uncertainties persist, a nuanced approach to valuation and strategic deployment of capital emerges as a cornerstone for navigating the evolving landscape of mergers and acquisitions", adds Jan Brabec, partner in corporate finance at Deloitte's advisory and technology practice.

Global developments and politics continue to influence markets. The war in Ukraine continues and could reach a stalemate. There is also the threat that China may invade Taiwan and tensions in the Middle East have increased as a result of the conflict between Israel and Hamas. Although the impact of these geopolitical events on financial markets, supply chains, oil and other commodity prices is not precisely measurable, it is clear that the global economy is becoming more fragmented.

Despite rising global conflicts and political tensions, along with tight monetary policy, 2023 has evolved as a period of consolidation that has effectively averted a looming economic recession. Relatively stable commodity prices played a key role in supporting disinflationary tendencies throughout the year. However, households and many businesses, particularly in Germany and the Central and Eastern Europe (CEE) region, faced persistent economic problems that constrained household consumption - the main driver of economic growth.

This problem is exacerbated by continued low consumer confidence, although there was an improvement last year compared to 2022. A combination of factors, including persistent inflationary pressures and a cautious growth outlook, negatively affected the economic environment throughout last year.

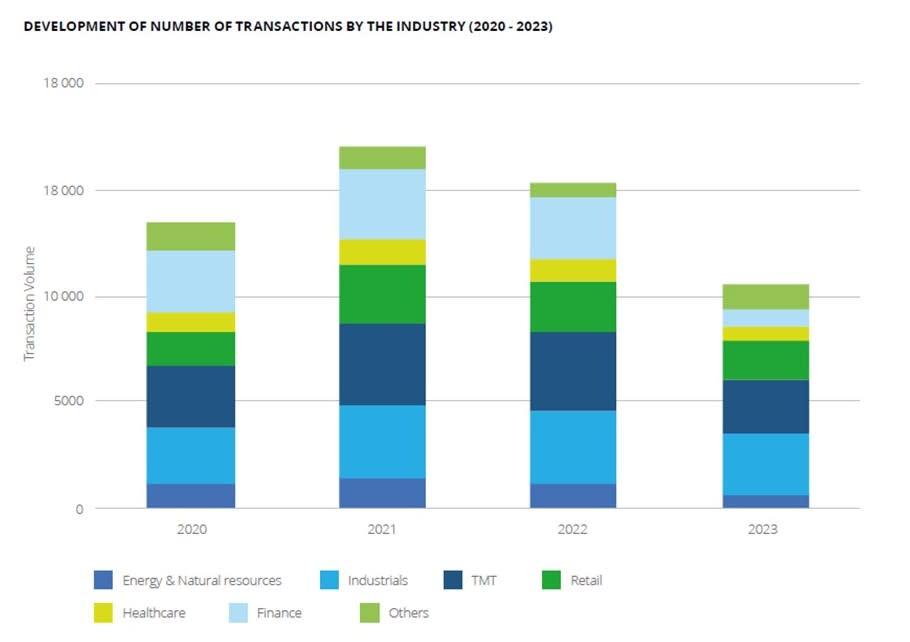

In addition, the number of transactions continued to fall over the past year, from 15,249 in 2022 to 11,629 in 2023, a 23.7% year-on-year decline, bringing the total volume of transactions close to pandemic levels. Furthermore, the total value of transactions has also seen a significant year-on-year decline, specifically by 34%.

The European market lagged behind both the US and global markets in terms of transactions last year, with the European market (EU27 + UK) down 23.7% compared to the global market, which fell 20%, and more significantly behind the US market, which fell 13.5% over the same period. The overall decline in market activity can be attributed to higher interest rates, continued geopolitical tensions and a generally negative economic outlook in Europe.

With the exception of Bulgaria and Luxembourg, all European M&A markets have seen a rapid decline in the number of transactions. The most affected regions were Cyprus (-53.7% yoy), Malta (-46.2% yoy) and Lithuania (-40.6% yoy). Germany and France saw a drop of around 30% in the number of transactions and other major European markets (Italy, UK and Spain) saw a drop of around 20%.

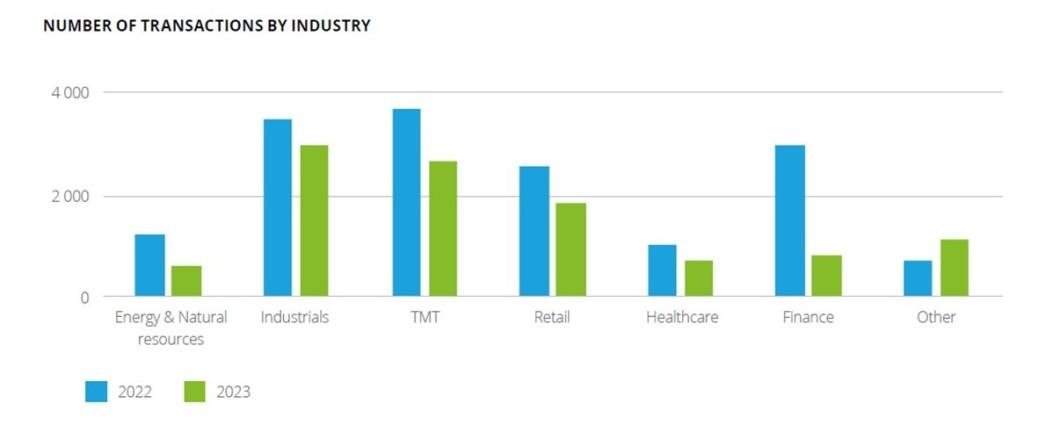

The manufacturing industry continued to dominate M&A activity, accounting for 28% of the total number of transactions last year. It was closely followed by the technology, media and telecommunications (TMT) sector with 25%, and the retail sector moved into third place with 17%. Conversely, the financial sector saw the largest decline in the number of transactions between 2022 and 2023, from 19% to 8%.

The full M&A Index, which includes a comprehensive summary for 2023, can be downloaded here:

M&A Index Q1 2024:

In Pursuit of Value

Deloitte M&A index is a forward-looking indicator that forecasts future M&A deal volumes – the number of announced transactions over the observed period – and identifies the key factors influencing the dealmaking conditions on the European Market (characterized as 27 countries of the EU + the United Kingdom). Compiling data from various global databases, including Capital IQ, Mergermarket, Pitchbook, Eurostat, and many more, the model utilizes a combination of statistical and algorithmic tools to provide a comprehensive review of the M&A market activity. The Index is created from a composite of market indicators – specifically pertaining to macroeconomic reality, liquidity, and general market dynamics. These variables are then tested for statistical and economic significance to M&A market volumes. The result is a dynamic, evolving, and up-to-date model allowing Deloitte professionals to accurately access and analyze factors influencing M&A market activity, as well as predict – with a high degree of certainty – the market activity in subsequent periods.

EQT raises €22 billion for latest PE fund

27 February 2024

Capital One to buy Discover for $35 billion

21 February 2024

A new edition of the M&A index is being prepared

16 February 2024

Private Equity Confidence Survey Central Europe 2024

9 February 2024

M&A: How was 2023 and what will 2024 bring?

4 January 2024

Deloitte is the top financial advisor in CEE

1 December 2023

PE fund KKR to buy the rest of Global Atlantic

30 November 2023

Financial Advisory Digital Family

27 November 2023

2024 investment management outlook

22 November 2023

Deloitte M&A Index 2023 Q3-Q4

13 November 2023