22 June 2022

Carbon-proofing the grid: Increasing renewables and resilience

How power companies can prepare for 2035 by investing in flexibility today

With the threat of climate change, it behooves utilities to consider doubling down on carbon mitigation and adaption–especially as the cost of carbon-proofing is lower than the cost of inaction for utilities and their customers. The power sector is both a primary mover and a casualty of carbon emissions. Power companies drive the clean energy transition: Their move to lower-carbon sources of generation and higher efficiency enables the decarbonization of all electricity-consuming sectors. At the same time, power companies are most vulnerable to the effects of the carbon accumulated in the atmosphere, facing higher exposure to physical risk from climate change than other sectors. As a result, they have much to gain or lose in their quest to decarbonize while parrying climate blows. Most utilities have set targets to fully decarbonize by mid-century and are implementing strategies to achieve those targets and prepare their workforce for the transition.

Over the past year, it has become more apparent that the power sector will likely need to more than redouble its efforts. We have reached what the UN Secretary-General has called “code red for humanity,” based on the Intergovernmental Panel on Climate Change’s latest report that the world is quickly approaching the 1.5-degree tipping point. The Biden administration has made pledges nationally and internationally that would require full decarbonization of the power sector by 2035—a milestone around which there is consensus across pathways to limit global warming to 1.5 degrees (see sidebar, “Pathways to decarbonization”).

With the carbon goalposts shifting, how can utilities prepare the grid for accelerated decarbonization targets amid aggravated climate change effects? And how can they do so while maintaining reliability, affordability, and safety in a context rife with other challenges, such as increasing demand, market disruption, and cybersecurity threats?

Utilities should invest in “carbon-proofing” the grid today to have the flexibility needed in 2035 in a decarbonized scenario. Carbon-proofing generation, transmission, and distribution has two mirror goals:

(1) removing carbon from the grid; while

(2) protecting the grid from carbon already locked into the atmosphere.

First, our analysis will show that the cost of carbon-proofing the grid is lower than the cost of doing nothing across all regions according to utility calculations in their Carbon Disclosure Project (CDP) filings. Moreover, many utilities have underestimated the cost of some carbon-related risks, suggesting that the delta between the costs of action and inaction is even greater than the estimates. A second finding is that flexibility measures that can help meet both carbon-proofing goals—renewables deployment and resilience to extreme weather and climate events—are no-regrets investments. Finally, the analysis will explore how a new “carbon compact” between utilities, regulators, and customers can help unlock the necessary funding by aligning capital investment decisions with carbon-proofing at the lowest cost to customers.

Pathways to decarbonization

National and global full-decarbonization scenarios show many pathways to full decarbonization, hinging on the extent of electrification, solar and wind generation, and biomass utilization. The landmark Princeton University Net Zero America study outlines the options for the United States and identifies three focus areas in the 2020s that appear across all pathways:

- The first is an acceleration of massive wind, solar, electric vehicle (EV), and heat pump deployments. More specifically, it involves the deployment of over 3 million public chargers to accommodate 50 million EVs on the road, a doubling and tripling in the respective shares of residential and commercial electric heat pumps, and a quadrupling in wind and solar capacity to supply half of US electricity.

- The second area is investment in transmission and carbon dioxide (CO2) pipeline infrastructure. This includes increasing high-voltage transmission capacity by 60% to connect new renewables with demand centers.

- The third is investment in research, development, and deployment (RD&D) for technologies that need to start operating in the 2030s, notably “firm” electricity technologies such as long-duration storage.

The cost of carbon-proofing the grid can be lower than the cost of doing nothing

Publicly available utility CDP disclosure calculations show that utilities have calculated the cost of action as lower than the cost of doing nothing to address climate change. Indeed, most investor-owned utilities (IOUs) now voluntarily disclose climate-related risks and opportunities to the CDP, along with estimated costs.

Our analysis considers all 29 publicly available IOU disclosures covering 2020, a year when the United States saw a record annual drop in greenhouse gas emissions amid the global pandemic. The year 2020 also saw record extreme weather events and damage to utility infrastructure that brought climate concerns to the fore. Climate disasters costing at least US$1 billion each reached a record-high 22 events costing over US$100 billion, wildfires burned a record acreage, and a record number of tropical cyclones made landfall.

Utilities prepared and submitted these disclosures in 2021, the same year that the Biden administration announced a net-zero target for the United States and signed into law the Infrastructure Investment and Jobs Act funding some of the investments needed to achieve this target, while the Glasgow agreement provided a global consensus call for action on climate change. And in 2021, US$1 billion-plus climate disasters reached another record, topping over US$145 billion in cost.

To what extent did these 2020 and 2021 events shape utility climate risk assessments?

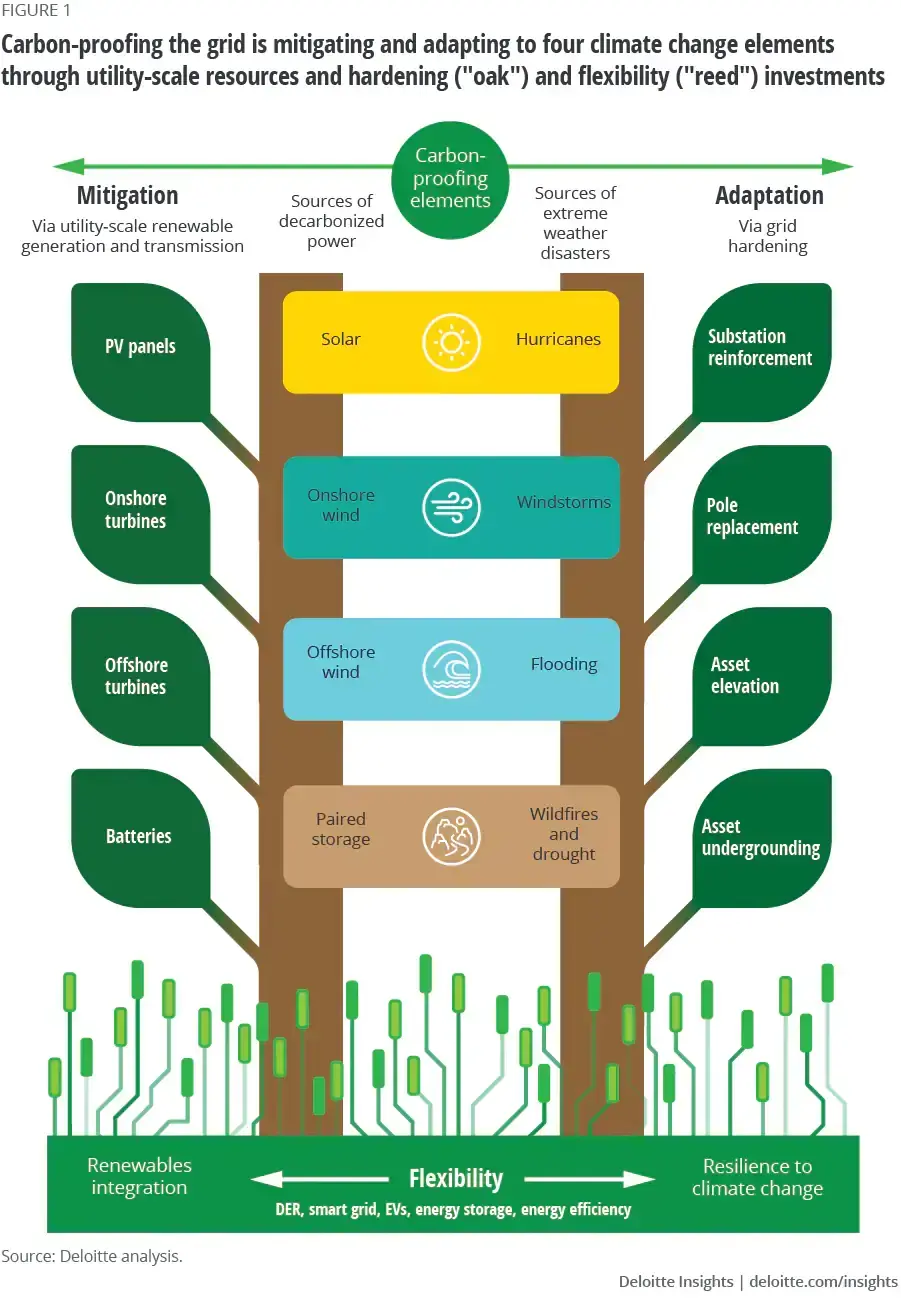

Deloitte developed a framework to help assess how the 29 IOUs that disclosed to the CDP in 2021 qualified and/or quantified climate-related risks and opportunities (figure 1). Organized around the two carbon-proofing goals, the mitigation side shows the leading technologies associated with decarbonization, while the adaptation side shows the major types of grid hardening technologies deployed to guard against the extreme weather events that have been increasing in frequency, severity, and attributability to climate change. Flexibility technologies that can both integrate renewables and increase resilience undergird the carbon-proofing.

The framework furthermore draws on La Fontaine’s fable about the oak and the reed to illustrate how a combination of large-scale and smaller distributed resources are needed to create a renewable and resilient grid. The oak is massive, but ultimately proves to be brittle during an epic storm, while the comparatively miniscule reed withstands the storm because it can bend. This is also a useful metaphor for the different types of carbon-proofing investments. Carbon-proofing the grid will require both “oak” and “reed” investments. Utility-scale grid development and hardening are the “oaks.” On the mitigation side, a record buildout of utility-scale wind and solar generation, storage, and transmission and distribution (T&D) would be needed to achieve decarbonization targets. On the other side of the carbon-proofing equation, system hardening, such as undergrounding T&D lines, enables utility infrastructure to withstand extreme weather events. But there is only so far the utility-scale investments and hardening can go; hence the need for “reeds” too. We are already running up against the grid’s ability to integrate renewables and recover from extreme weather events when damage occurs. Massive capital investments may also face resistance from regulators reluctant to pass the cost along to customers in the form of higher rates if lower-cost alternatives to grid expansion and hardening are available. Finally, decade-long implementation timelines to permit and build a transmission project could impede rapid decarbonization timelines.

Reeds are distributed energy resources (DERs) that can follow load, and the supporting digital infrastructure, including technologies that can harness the DER in optimizing and balancing the grid via demand response, real-time flexible load programs, managed EV charging, and eventually vehicle-to-grid and transactive energy programs. These flexibility resources can be aggregated into microgrids and “bend but not break” by sectioning off from the grid in the event of an outage and continue powering critical infrastructure. They can be more rapidly deployed to help align demand to renewable supply, offer nonwire alternatives to T&D buildout, and provide ancillary services to the grid, such as frequency regulation, voltage support, and black starts.

Our framework considers mitigation and adaptation costs across four elements—sun, wind, water, and earth. Sun refers to solar radiation as the source of the fastest growing decarbonization technology (solar power) and a climate risk that occurs when solar radiation peaks (hurricanes). Wind is both a source of power generation and storms. Water refers to offshore power and climate risk sources, namely offshore wind power and flooding. Finally, earth encompasses the battery storage increasingly paired with solar on the mitigation side, and drought and wildfires on the adaptation side.

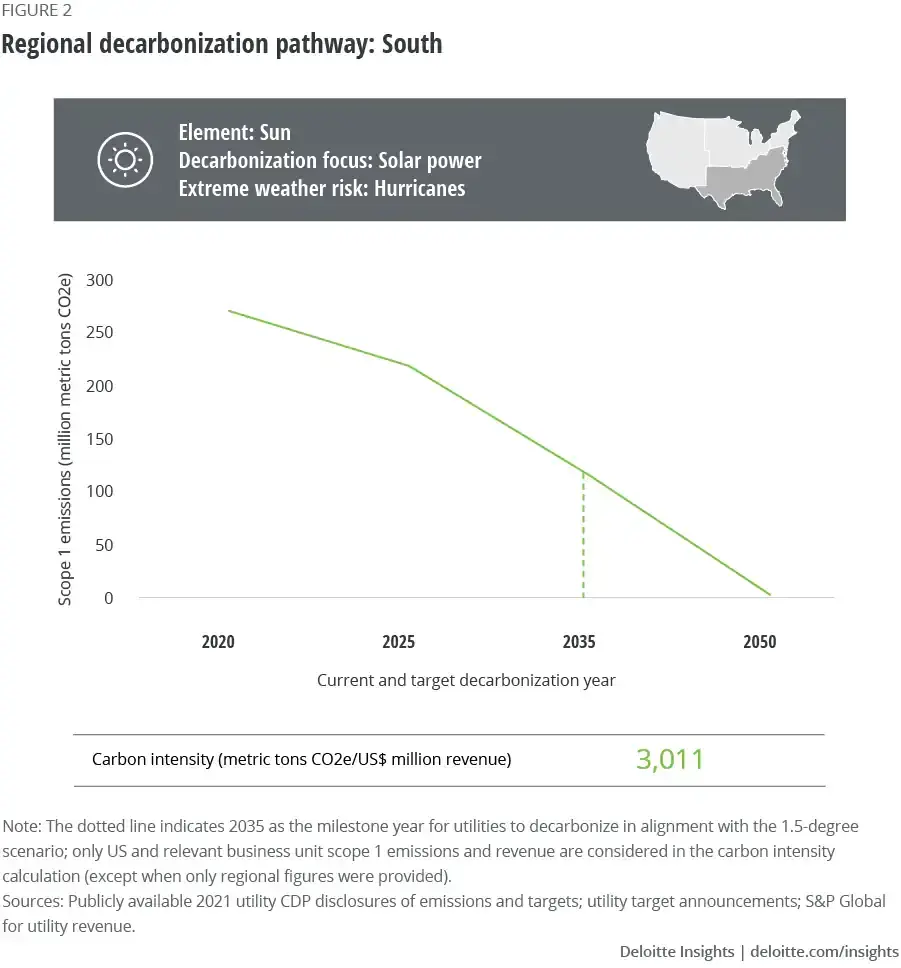

The sun, wind, water, and earth elements also map fairly well to the four US Census regions. While most utilities are deploying multiple renewable technologies and climate mitigation technologies, focus areas are apparent in each region. Similarly, the adaptation technologies mentioned are not exclusive matches—for example, undergrounding assets works not only for wildfires but also for hurricanes and storms—but rather reflect the most prominent adaptation technology mentioned for each region’s respective primary climate risk. Of the eight risk types the CDP identifies—current regulation, emerging regulation, technology, legal, market, reputation, acute physical, and chronic physical—utilities operating in the South have largely focused their decarbonization efforts on deploying solar, and their top climate concerns often revolve around hurricanes. Midwestern utilities’ carbon mitigation and adaptation tend to revolve around wind power and the storms, derechos, tornadoes, blizzards, and extreme cold temperatures that winds blow into the region, while their Northeastern counterparts are pioneering US offshore wind development while mainly focusing on rising sea levels and flooding concerns. Finally, utilities in the West are quite advanced in combining solar with storage and deploying potentially mobile storage in the form of EVs, while their leading climatic concern is wildfires. Utilities in the South have largely built their decarbonization strategies around a bountiful resource in the region—solar—and according to their CDP filings seem most concerned about shielding their assets from the hurricanes that regularly pound their coastline. But many utilities in the region have not taken full advantage of the region’s natural solar resources as they remain more reliant on fossil and nuclear power compared to other regions. The fossil reliance yields have a relatively high carbon intensity, with utilities averaging 3,011 metric tons (MT) of CO2e per million dollars of revenue, and with no utilities having announced a net-zero target before 2050 (figure 2). As a result, the utilities’ aggregated pathways suggest emissions could be over 100 million MT in 2035.

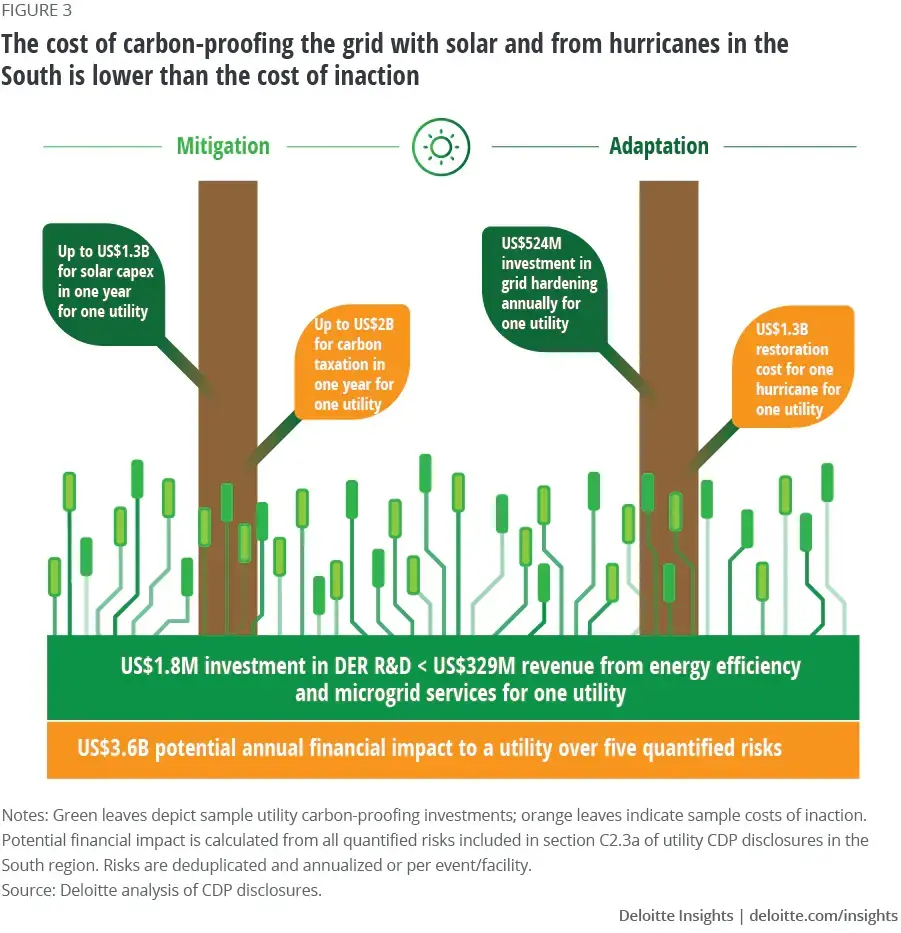

Figure 3 shows the cost of carbon-proofing action and inaction based on the potential financial impact of climate risks that utilities identified in their CDP disclosures versus their estimated cost of responding to the risk. The solar capex that utilities in the South are planning—for example, totaling as much as US$1.3 billion for just one utility in one year—falls well below the utilities’ quantified billion dollar-plus costs of inaction. And estimated potential carbon taxation could cost a single utility billions in just one year. Similarly, moving to the adaptation column of the figure, given the billion-plus cost of restoration after a hurricane, grid-hardening costs below that threshold could be worth the investment. While probability assessments for these risks vary, the probability increases exponentially the longer action is delayed.

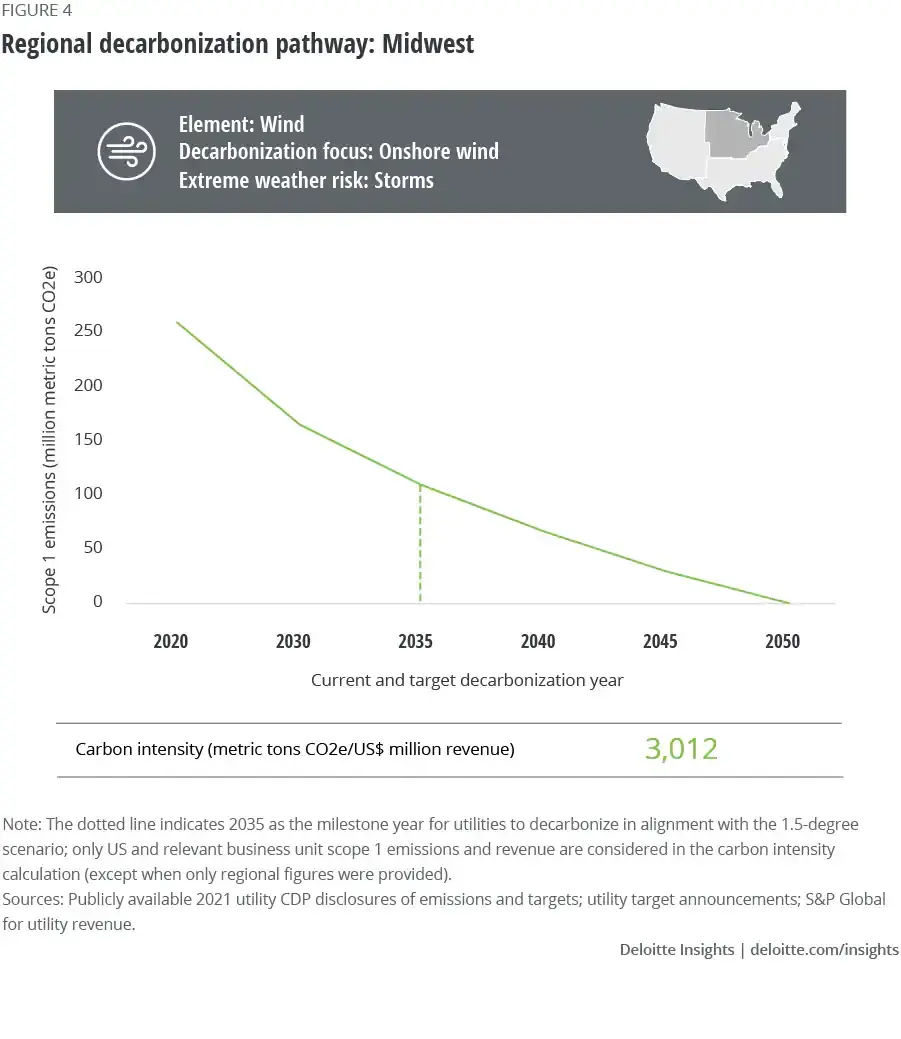

The Midwest has a similar emissions profile to the South, but close to half of the Midwestern utilities have more ambitious targets to make a significant impact by 2030 and/or decarbonize by 2040/2045 (figure 4). Like the South, they have harnessed their greatest renewable resource, in this case wind, from which they also need to protect their assets when it combines with storm conditions.

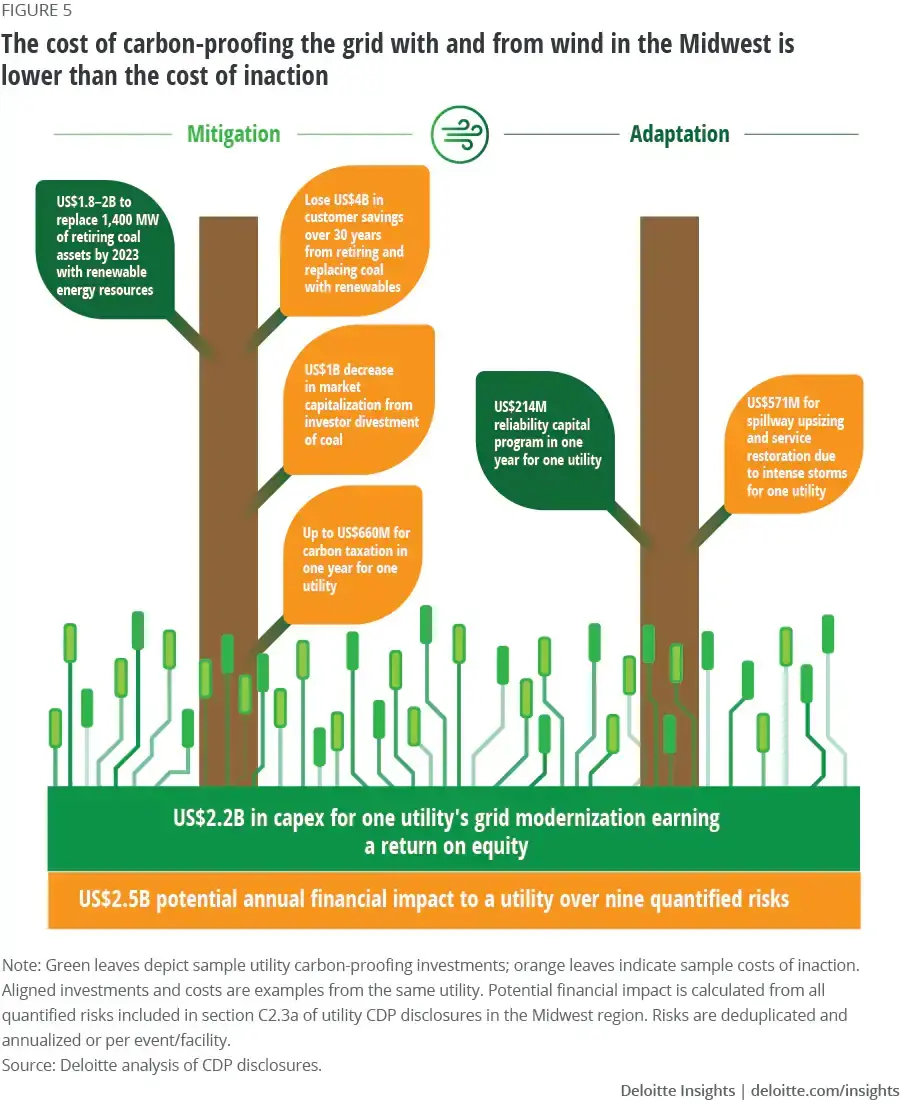

In the example of one utility, replacing coal assets with wind power would not only provide value for shareholders, but could also yield as much as US$4 billion in customer savings over the net-zero-by-2050 timeframe (figure 5). Meanwhile, inaction could cause up to a US$1 billion decrease in market capitalization and a simultaneous increase in carbon taxation—estimated at US$660 million for one utility in one year. On the adaptation side, annual investment in reliability may be less costly than infrastructural changes and service restoration in response to intense storms.

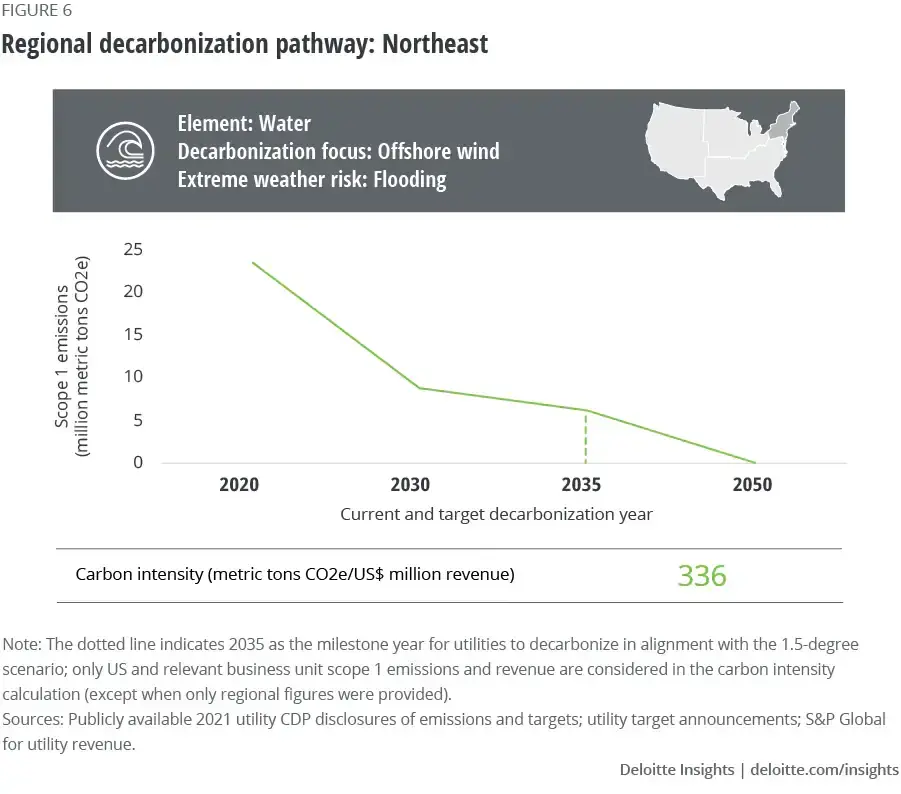

Northeastern utilities most closely hew to the 2035 decarbonization pathway, with most of our sample being on track to fully decarbonize by then (figure 6). The Northeast is at the forefront of the offshore wind industry’s takeoff in the United States. The region’s utilities also consider their greatest risk offshore: rising sea levels and flooding.

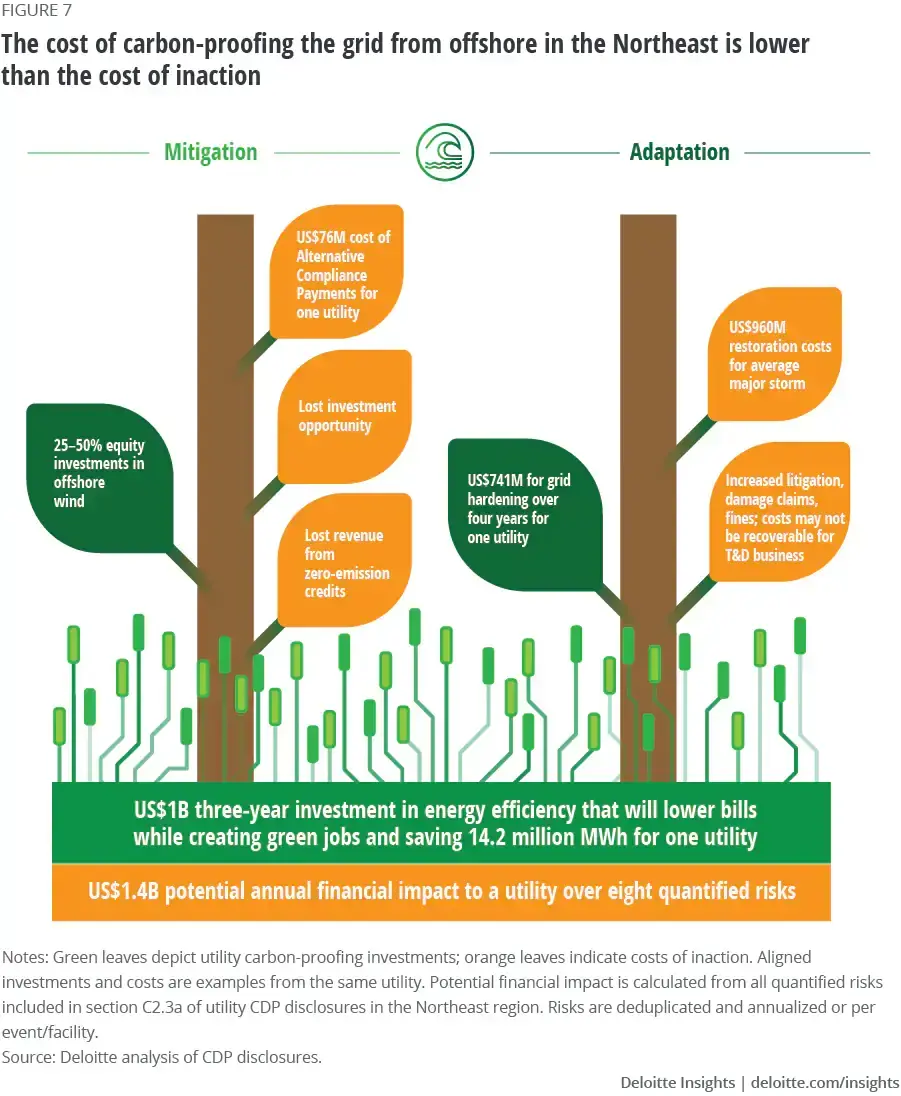

Many northeastern utilities are allying with more established industry players to deploy offshore wind via equity investments ranging from 25% to 50% (figure 7). Remaining on the sidelines could mean missing opportunities to invest in a fledgling industry that could require US$12 billion in capex annually according to an estimate by the Biden administration, and increase the chances that utilities would fall short of meeting targets. Missing targets might incur alternative compliance costs. Annual grid-hardening costs could be lower than restoration costs for an average major storm.

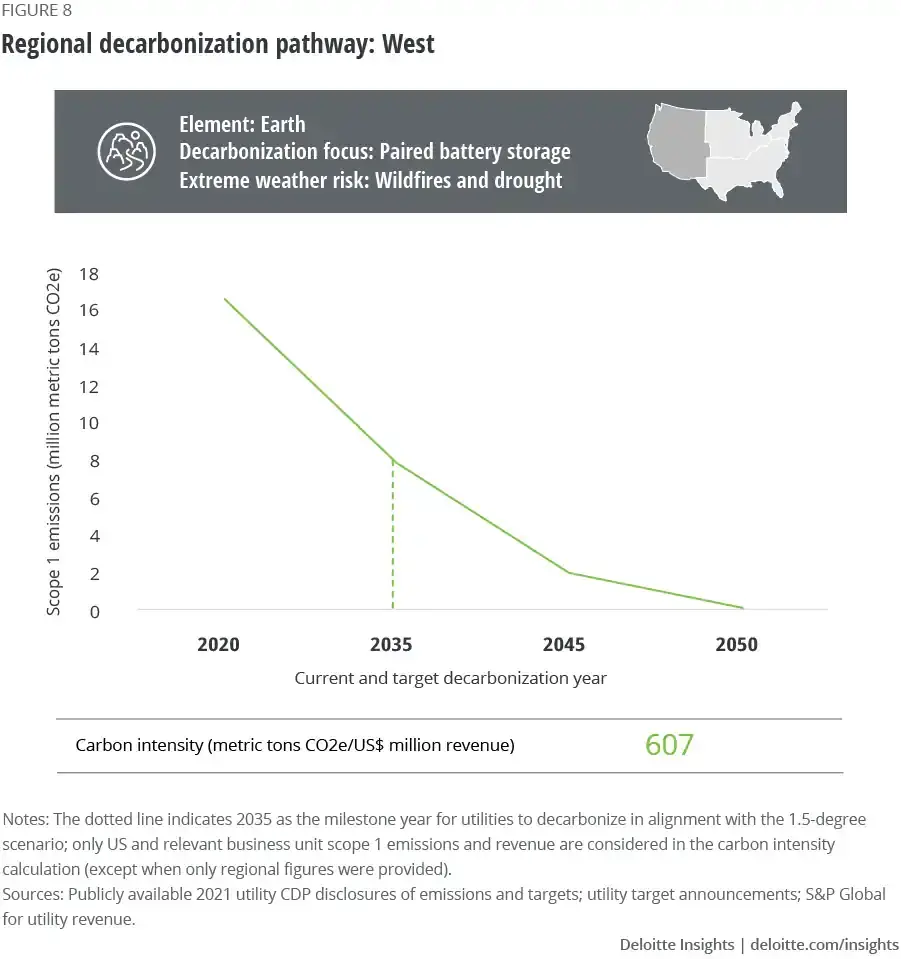

Utilities in the West region especially focus on battery storage in both stationary and EV form on the decarbonization side of the equation, and on wildfire prevention as the primary focus for carbon adaptation. Utility emissions targets are more closely aligned to the administration's 2035 electricity decarbonization target, given that California has a 2045 statewide 100% clean electricity target (figure 8).

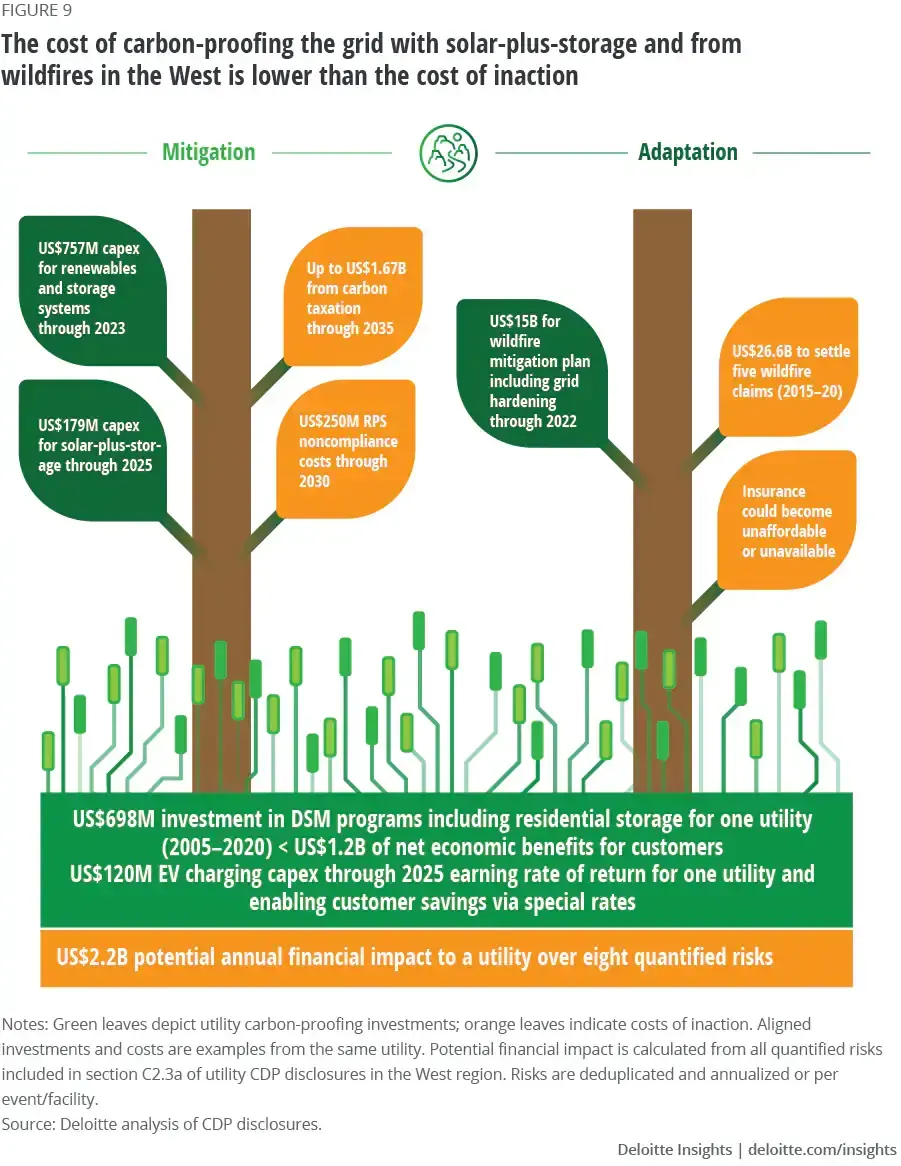

Estimated capex for renewables and storage is lower than the steep anticipated carbon taxation and Renewable Portfolio Standard (RPS) noncompliance costs utilities might face through 2035, not to mention their exposure to expected fossil fuel price increases (figure 9). While wildfire mitigation plans are costly, the rising cost of settling wildfire claims is anticipated to be even higher. Moreover, the combination of the two could cause insurance rates to rise for many utilities, affecting their operations and increasing customer costs, as utilities noted in their CDP disclosures.

The delta between action and inaction costs may be higher than estimated

Many utilities have underestimated the cost of carbon-related risks in their carbon disclosures. The incorporation of these risks shows that the delta between the costs of action and inaction could be even greater than utility estimates. Many utilities have not fully considered the cost of physical climate and regulatory risks, and are basing assumptions on historical trends, which, as 2020 and 2021 have shown, might no longer be reliable indicators of future trends. The geographies of various extreme weather event risks also seem to be changing. Some utilities that have not traditionally needed to prepare for certain types of extreme weather events may need to expand their risk hedging portfolio, such as utilities in Texas reconsidering winterization strategies. Furthermore, some solutions have trade-offs related to this changing risk geography. For example, undergrounding can be highly effective in preventing wind damage but is vulnerable to damage from heat waves and more time-consuming and costly to install and repair.

Many utilities also appear to underestimate cybersecurity risk in their CDP disclosures. None of the 29 utilities identify it as a stand-alone risk in their organization’s climate-related risk assessments. Of the seven utilities that mention cybersecurity in the context of other risks, most do so in relation to technology risks. Renewables have not been subject to the same degree of cybersecurity regulation as traditional generation because they have historically been considered “low impact” or out-of-scope under the North American Electric Reliability Corporation (NERC) risk classification. Historically, renewables have been built speed-to-value when compared to traditional transmission and generation facilities. For example, less secure communication protocols and/or limited physical security measures are often implemented. As the growth of renewables continues to accelerate, more traditional cybersecurity regulations are expected to apply as they become an increasingly significant part of the overall generation portfolio. Developers should consider cybersecurity and related regulatory implications early in the design process to ensure compliance and avoid the need for remediation later.

There is also a stranded asset risk for natural gas infrastructure. Most of the 29 utilities report planned capex in fossil fuel generation, including investment in new natural gas-fired generation, without specifying a decarbonization pathway such as transition to renewable natural gas or convertibility to hydrogen.

Finally, few of the 29 utilities have quantified their earnings at risk should carbon pricing come into effect as countries and companies seek to align with the 1.5-degree scenario. Deloitte analysis, assuming carbon pricing consistent with a 1.5-degree scenario according to Wood Mackenzie (US$160/MT), estimates the cost of carbon emissions for utilities based on their current trajectory could reach US$57.3 billion in 2030 in the absence of action—equivalent to 89% of FY2021 EBIT for the 29 utilities (for more on carbon pricing, see the section “New carbon compacts between utilities, regulators, and customers can enable carbon-proofing”).

The “reeds” that meet both carbon-proofing purposes tend to be no-regrets flexibility investments

The utilities’ CDP disclosures also show that the “reeds” that meet both carbon-proofing goals tend to be no-regrets investments because they enable both increasing the share of renewables on the grid and keeping the lights on when extreme weather damages the grid. While utility-scale “oak” decarbonization investments and hardening measures mostly appear in utilities’ risk assessments, with quantifiable or qualifiable costs and benefits, most of the flexibility investments appear to be in the section where utilities identify climate-related opportunities. For example, one utility estimated that a US$1.8 million R&D investment in DER, storage, and renewables yielded US$329 million in revenue from energy efficiency and microgrid services, and another that a US$698 million investment in demand-side management (DSM) programs can deliver US$1.2 billion of net economic benefits to customers (see figures in the previous section, “The cost of carbon-proofing the grid is lower than the cost of doing nothing”).

When DER are deployed as part of capex, they can earn a return for the utility, while lowering costs for customers and creating jobs—all while contributing to, and shrinking the cost and timeline of, decarbonization and climate mitigation.

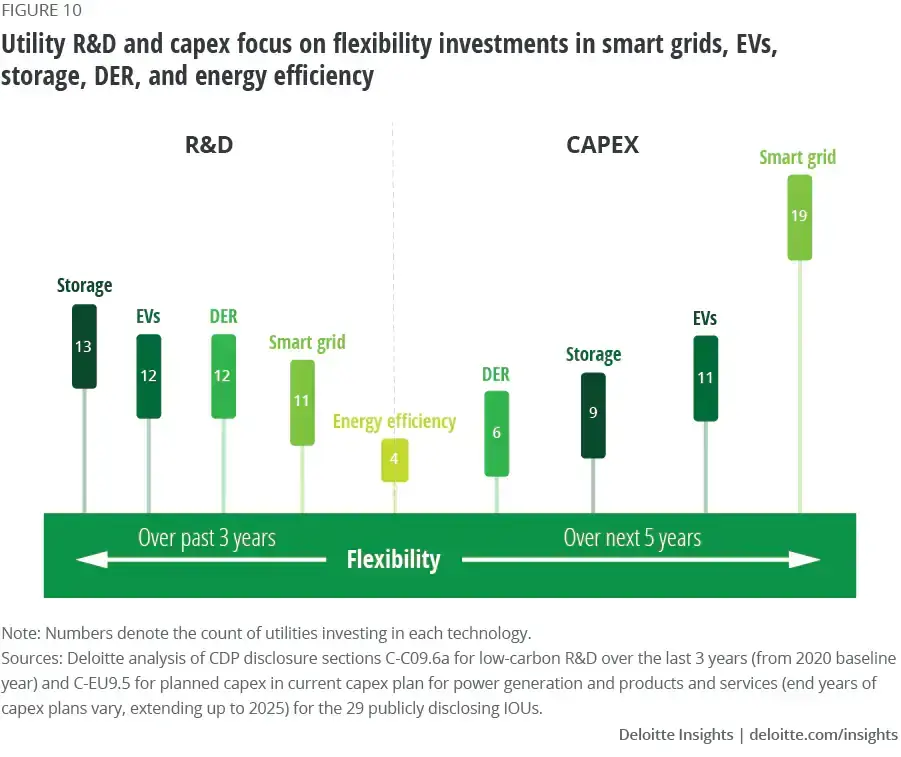

Most of the 29 utilities have recognized this win-win proposition and have focused their low-carbon R&D in flexibility investments over the past three years (figure 10). Energy storage has been the largest area of activity, followed by EVs, DERs, smart grid, and energy efficiency. Utilities’ planned capex in upcoming years shows a focus on the smart grid undergirding all flexibility technologies, followed by EVs, storage, DER, and energy efficiency.

New carbon compacts between utilities, regulators, and customers can enable carbon-proofing

The utility regulatory framework will have to accommodate the cost of carbon-proofing solutions, while maintaining customer affordability thresholds. Different ratemaking approaches may need to be considered to incentivize “reed” investments, versus some of the more traditional “oak” investments, while allowing the utility to recover the cost of its investment and any carrying charges, if necessary. Any such ratemaking changes could be impactful to the accounting for these investments and should be actively considered.

Performance-based ratemaking could similarly help utilities evolve new business models by better aligning regulatory incentives with decarbonization, resilience, and flexibility goals, as well as improved customer service. Beyond ratemaking, some states incorporate DER in their RPS policies. For example, Arizona’s RPS requires 30% of a utility’s requirement be met with DER, and further specifies that half of the DER be located in the residential customer segment. On the demand side, dynamic pricing could help increase commercial, industrial, and residential DER enrollment in demand response and managed EV charging. Utility customers are also more likely to enroll in a demand response program if they purchase a smart device or EV charger on a utility marketplace and the device is pre-enrolled in the utility’s DR program. For example, some utilities offer smart thermostats to customers at no cost if they pre-enroll in a DR program. Finally, ancillary service markets could enable utilities to tap into more value streams from energy storage and capture its locational value.

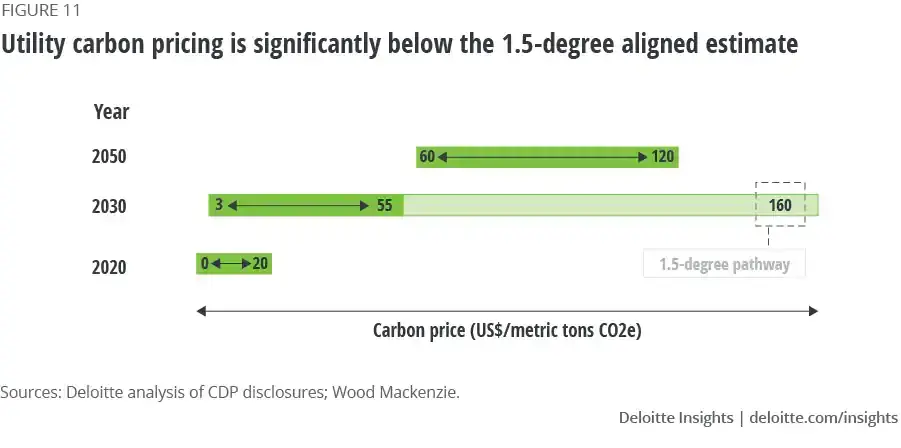

A sufficiently high carbon price could also quickly accelerate the pace of decarbonization by increasing the cost of inaction to a prohibitively high level. Of the 29 CDP-disclosing IOUs, 11 already participate in a carbon pricing system, and 16 anticipate being regulated by one in the next three years. Even more are already preparing for this scenario: Twenty-one of the utilities have an internal price on carbon, and five additional utilities are planning to use an internal price in the next two years. The primary reason utilities provided for implementing an internal price on carbon is to help them navigate existing and potential greenhouse gas regulations. Other top reasons cited are to drive low-carbon investment, stress test investment, and meet stakeholder expectations. These carbon prices are currently low, topping out at US$20/MT, while utilities anticipate them rising to the upper bounds of US$55/MT in 2030, and US$120/MT in 2050. However, both the 2030 and 2050 upper bounds fall below estimated pricing alignment with a 1.5-degree scenario (figure 11).

Utilities could also explore opportunities to develop new products and services to advance carbon-proofing objectives while minimizing costs to customers, especially the ones least able to shoulder them. For example, time-stamped renewable energy credits (RECs) could help customers achieve 24/7 goals. One utility developed an innovative 24/7 carbon-free energy agreement with a corporate customer, wherein it has committed to deliver at least 90% carbon-free energy on an hourly basis. On the residential customer side, opportunities include deepening the engagement of prosumers, who both consume and produce electricity, and reducing cost impact for low-income groups. For example, some utilities offer community solar and EV charging infrastructure programs specifically aimed to provide access for disadvantaged communities.

Conclusion

Utilities should consider “carbon-proofing” the grid today to gain the flexibility they will likely need in 2035 in a decarbonized scenario. Based on CDP filings, utilities have estimated that the cost of carbon-proofing action is ultimately lower than the cost of inaction across regions, technologies, and climate risks, and this delta is likely to increase. Even if the cost of decarbonization were higher than the cost of inaction, it might be worth pursuing, since any investment in mitigation would lower both the costs of action and inaction on the adaptation side of the carbon-proofing lever. Second, “reed” flexibility measures are no-regrets investments because they enable both decarbonization and resilience. Finally, a new “carbon compact” between utilities, regulators, and customers could help unlock the funding that will be needed by aligning capital investment decisions with carbon-proofing goals at the lowest cost to customers. Given the current climate calculus, utilities may do best to get into the reeds of preparing the grid for 2035.