24 May 2023

Deloitte M&A Index 2023 Q1–Q2

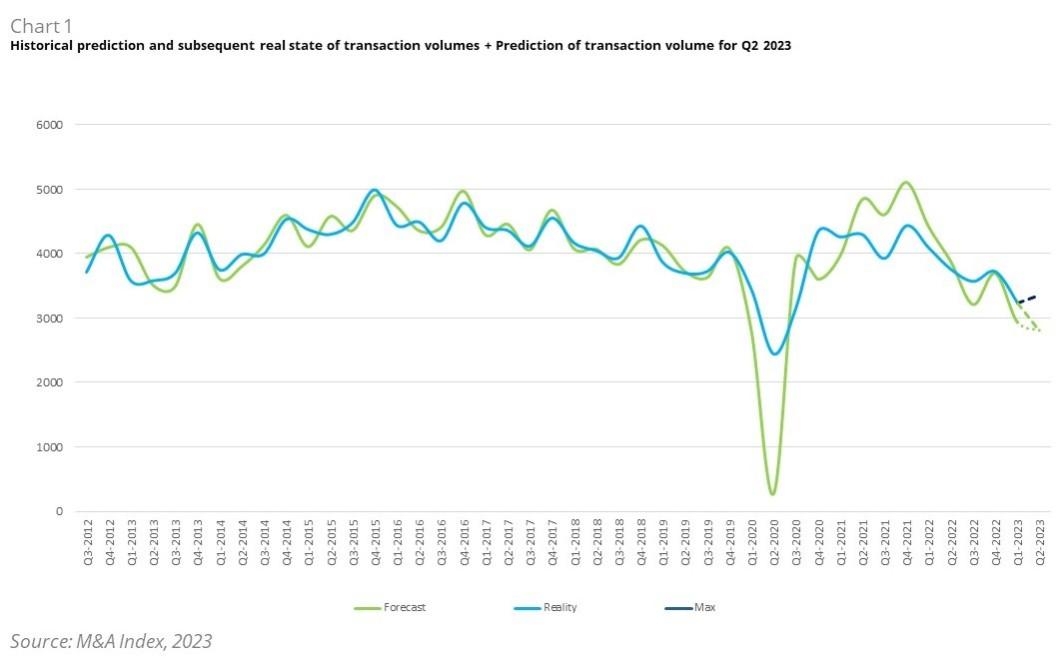

Number of European deals to fall by 13.3% in Q2 2023.

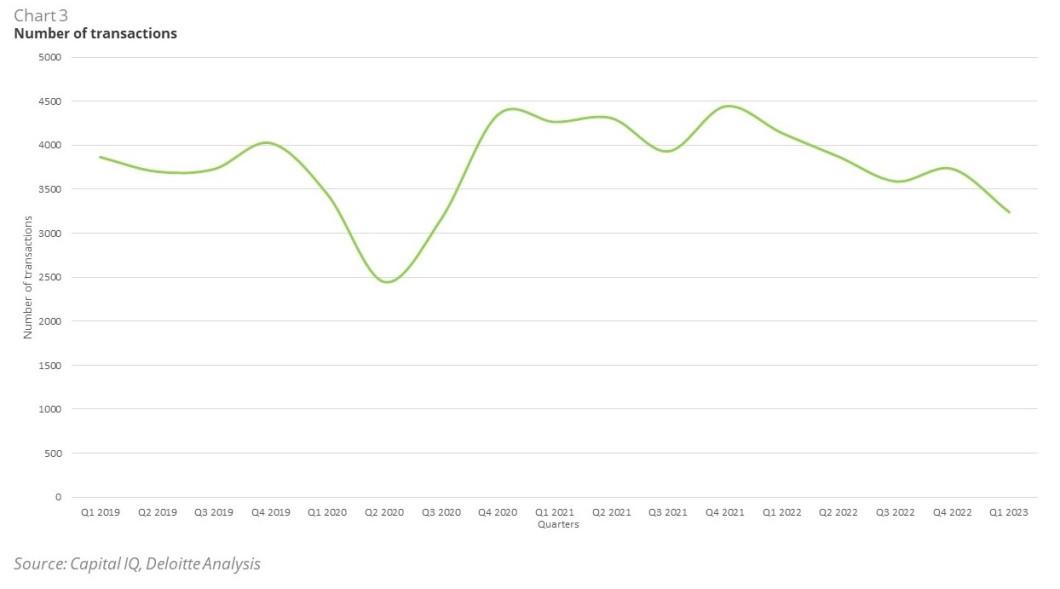

In the second quarter of 2023, the continued impact of negative macroeconomic factors such as persistent inflation, higher interest rates, slowing economic growth and continued supply chain disruption will result in a further significant decline in M&A activity. Turbulence in the banking markets and its impact on consumer confidence also contributed significantly to Q2 results. The Index forecasts 2,805 announced transactions for the second quarter of the year. In Q1 2023, the total was 3,237 transactions, so the model predicts a 13.3% decline. The model's optimistic scenario - which accounts for an unlikely, yet possible positive shock to consumer confidence and equity markets continues to allow for a potential modest 3.8% (q/q) increase in the number of market transactions. Thus, while we expect the number of M&A deals to slow in 2023, we believe the markets may still be eligible for a rapid recovery.

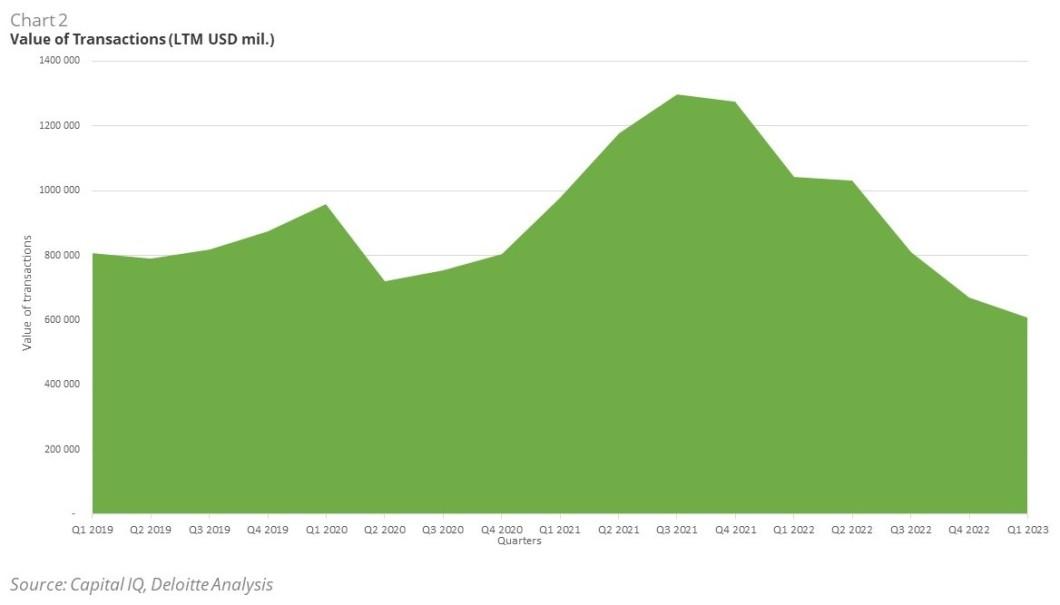

The total value of transactions (measured as the sum of the value of transactions executed in the last twelve months) also decreased, from USD 669 billion to USD 607 billion.

The prevailing geopolitical and economic uncertainty is expected to continue to influence market dynamics this year. However, there remains strong interest from strategic and financial investors in M&A involving significant targets in Europe. Going forward, investors are likely to focus on seeking investments in companies that have a significant market position, strong financial performance and a viable business strategy.

"Despite the cooling of the M&A market, there is still potential for a market recovery this year thanks to several factors, such as significant financial resources from private equity funds and strategic players, as well as the easing of the energy crisis," explains Jan Brabec, a partner in Deloitte's Financial Advisory Department.

Furthermore, investors are expected to carefully evaluate their corporate portfolios and consider divesting non-core assets as part of ongoing transformation strategies. In addition, the trend towards consolidation may continue, particularly in unexplored emerging market territories in Europe and elsewhere, presenting numerous opportunities for large-scale consolidation in the new economic reality. Continued economic uncertainty may present opportunities for acquisitions of companies in financial distress and buying opportunities for businesses looking to expand and grow. Over-indebted businesses may be available for acquisition at a reduced price at which more financially stable companies can buy them, thereby gaining access to new markets or technologies.

"Geopolitical and economic uncertainty continues to affect market dynamics this year, but signs of gradual stabilisation are emerging. Investors are looking for value in companies with strong market positions and business plans. Consolidation may continue in emerging markets, which brings many opportunities," adds Miroslav Linhart, senior partner in Deloitte's Financial Advisory practice.

Related articles

Japan's Topix stock index hits 33-year high

16 May 2023

Global IPO markets have cooled down

12 May 2023

European Venture Capital firms face capital shortage

25 April 2023

Opportunity funds fall out of favour

12 April 2023

Jet Investment expands to Poland

16 March 2023