MTX Group in talks to take over part of Aluflexpack

5 February 2025

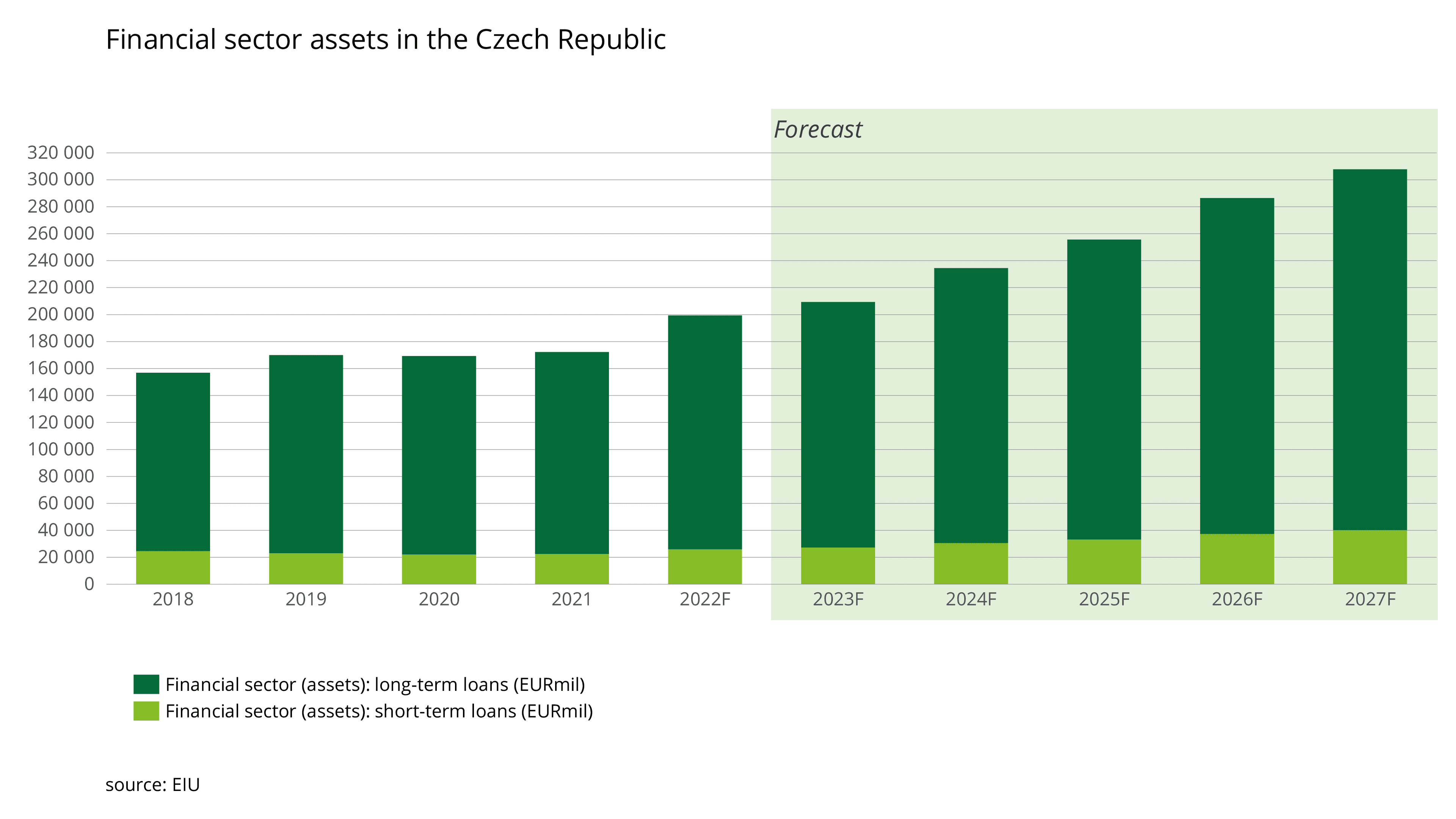

The financial sector in the Czech Republic has experienced growth in both long-term and short-term loan assets from 2018 to 2021, with a projected upward trend for 2022 to 2027. Long-term loans increased from €132,285.5 million in 2018 to €149,827.5 million in 2021. This growth is expected to continue, reaching €173,450.1 million in 2022 and €267,717.9 million by 2027.

Short-term loans also displayed a growth pattern, albeit with a slight decrease between 2018 and 2019. The value of short-term loans rose from €24,662.9 million in 2018 to €22,439.3 million in 2021. The future outlook for short-term loans shows a consistent increase, with projections reaching €25,977.2 million in 2022 and €40,095.9 million by 2027. The overall growth in both long-term and short-term loan assets indicates a healthy and expanding financial sector in the Czech Republic.

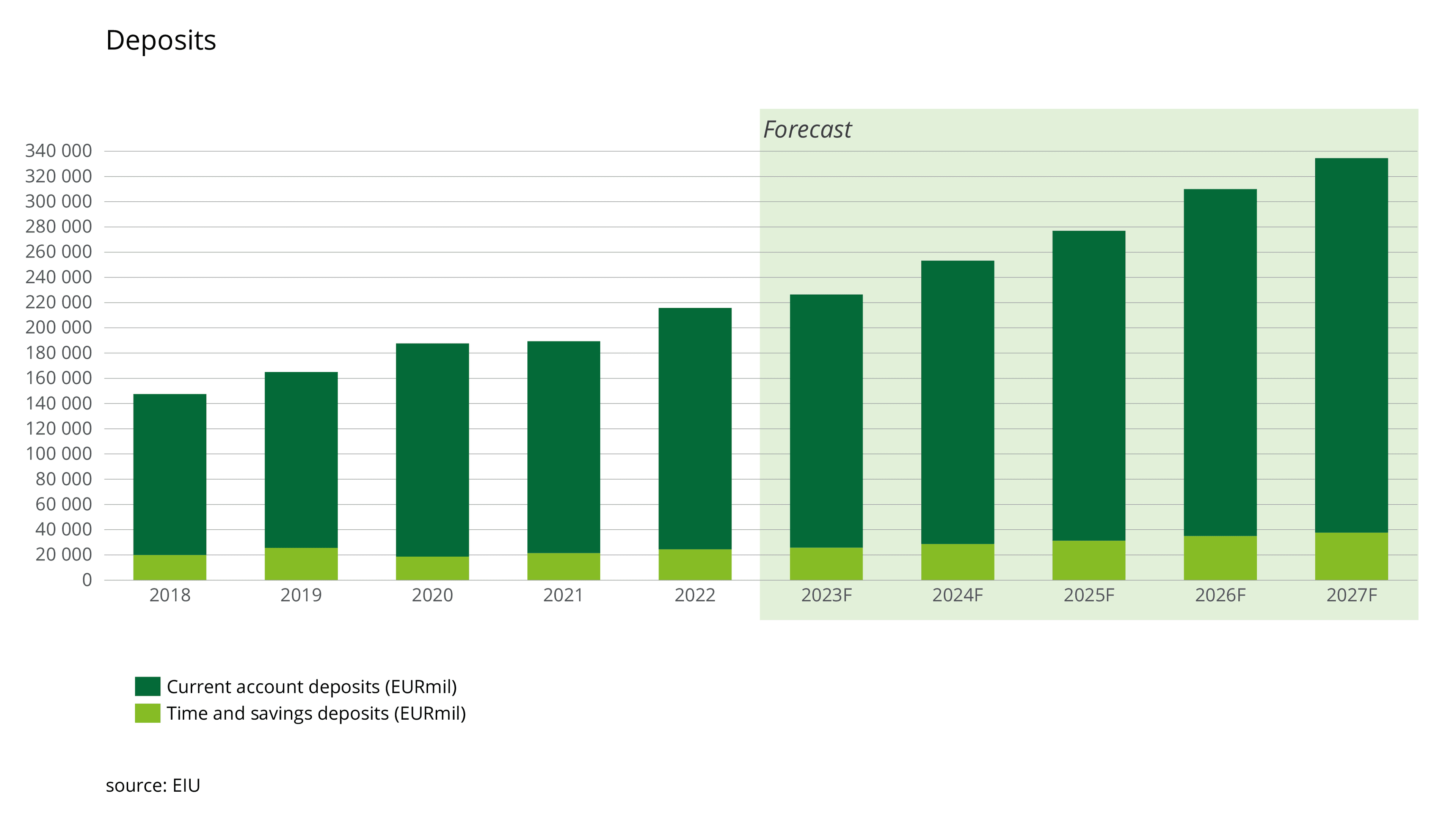

Deposits in the Czech Republic have experienced growth in both current account deposits and time and savings deposits from 2018 to 2021, with projections indicating continued growth from 2022 to 2027. Current account deposits increased from €127,603.7 million in 2018 to €168,081.5 million in 2021. This upward trend is expected to persist, with deposits projected to reach €191,358 million in 2022 and €296,771.1 million by 2027.

Time and savings deposits also exhibited growth, despite a dip in 2020. The value of time and savings deposits rose from €19,962.7 million in 2018 to €21,376.5 million in 2021. The future outlook for time and savings deposits is positive, with projections reaching €24,491.9 million in 2022 and €37,711.3 million by 2027. The overall growth in both current account and time and savings deposits signifies a robust and expanding financial landscape in the Czech Republic.

MTX Group in talks to take over part of Aluflexpack

5 February 2025

European CFO Survey autumn 2024

17 December 2024

AI in manufacturing

3 June 2024

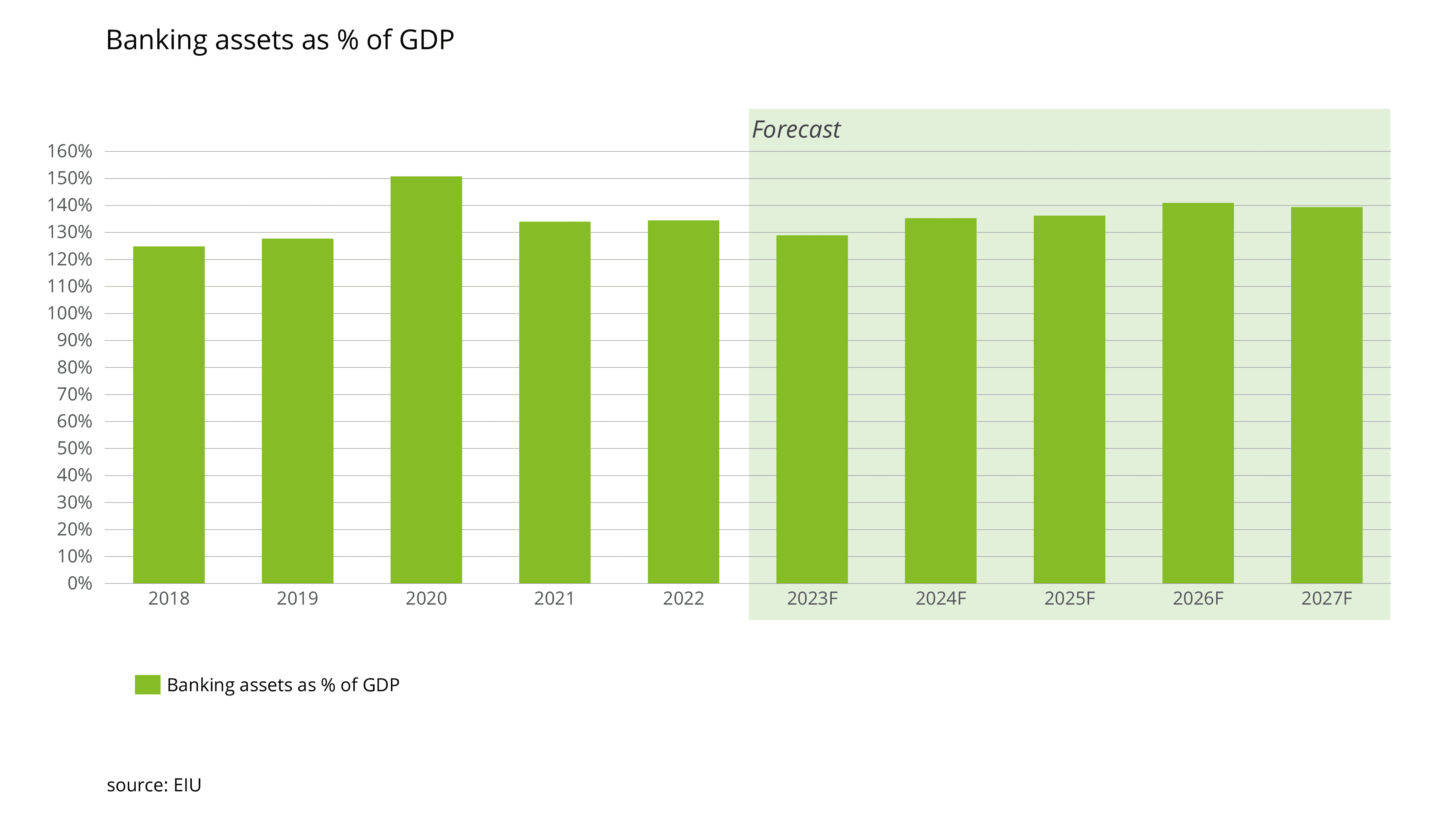

The Czech Republic's financial landscape has seen fluctuations in banking assets as a percentage of GDP, consistent growth in internet banking adoption, and dynamic interest rates for both lending and deposits. Banking assets as a percentage of GDP have experienced changes from 2018 to 2021, with projections indicating further fluctuations up to 2027. Meanwhile, the use of internet banking has steadily increased from 2011 to 2022, emphasizing the growing importance of digitalization in the banking sector.

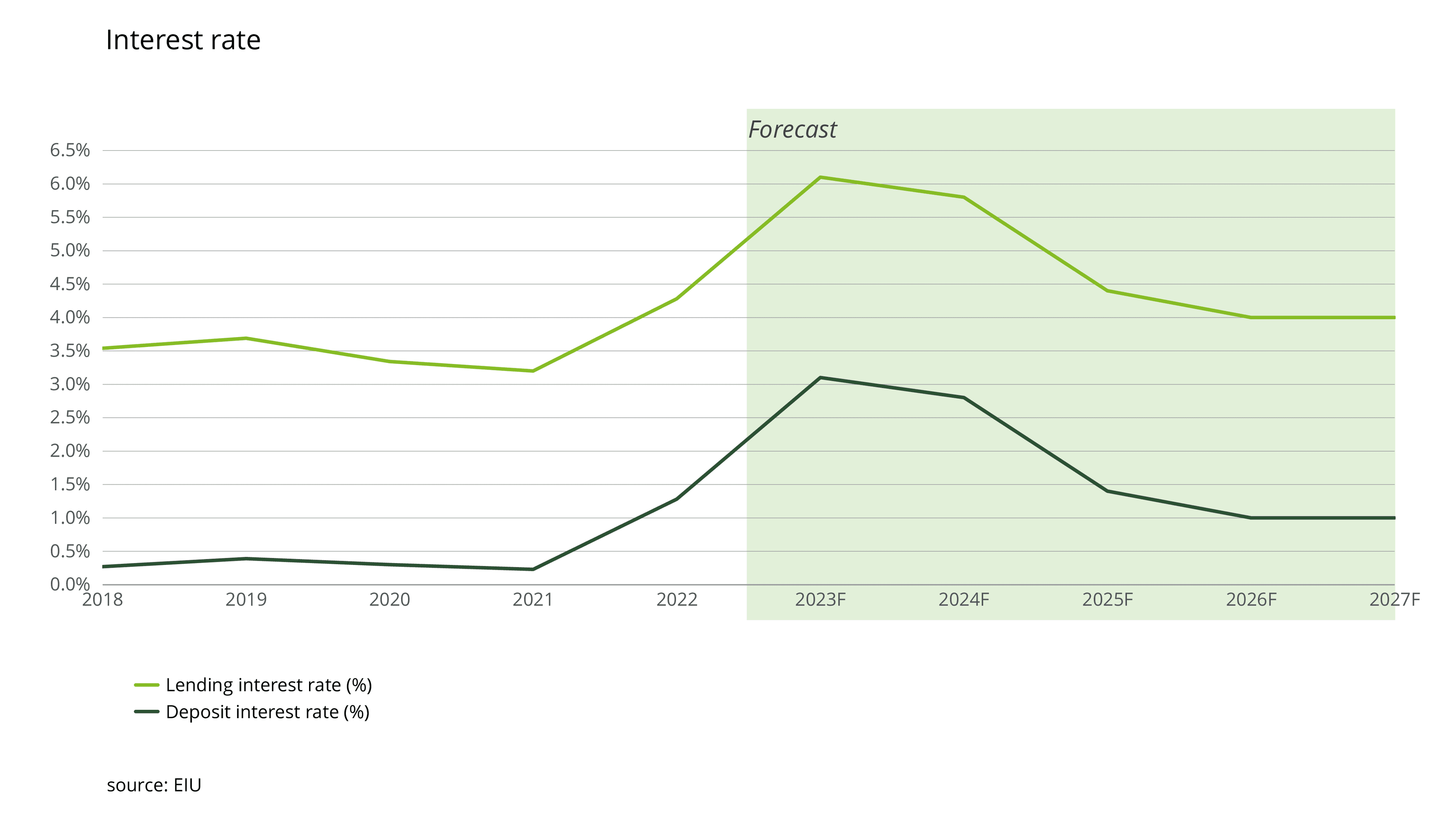

Interest rates have also seen fluctuations from 2018 to 2027F. Lending interest rates varied from 3.54% in 2018 to an expected peak of 6.1% in 2023F, stabilizing at 4% by 2026F and 2027F. Deposit interest rates followed a similar pattern, with an expected increase to 3.1% in 2023F before stabilizing at 1% for 2026F and 2027F. These changes highlight the dynamic nature of the financial market in the Czech Republic.