14 August 2023

Deloitte M&A Index 2023 Q2-Q3

As predicted in the previous edition of the M&A Index, the market cooled further in the second quarter of 2023, with the number of deals on the market approaching 2020 levels.

The second quarter was marked by the ongoing geopolitical crisis, rising interest rates, increased cost of capital, and tighter regulatory oversight, which posed significant challenges for investors and business owners alike; among other things, they faced declining valuations and were hesitant to commit to selling at prices below those in early 2022. In addition, the environment of soaring interest rates has effectively shut down the equity lending markets, severely limiting the viability of LBO investing (transactions in which a company is purchased by a financial investor, such as a PE fund, using outside funds) and therefore limiting the ability of investors to raise the necessary funds to execute large transactions. In a context of overall uncertainty and limited access to investment - factors that have been actively influencing M&A markets since virtually the end of 2021 - the Deloitte M&A Index for 3Q 2023 therefore forecasts a further, albeit more modest, decline in the number of announced transactions to 2,810, a decline of approximately 3.7%.

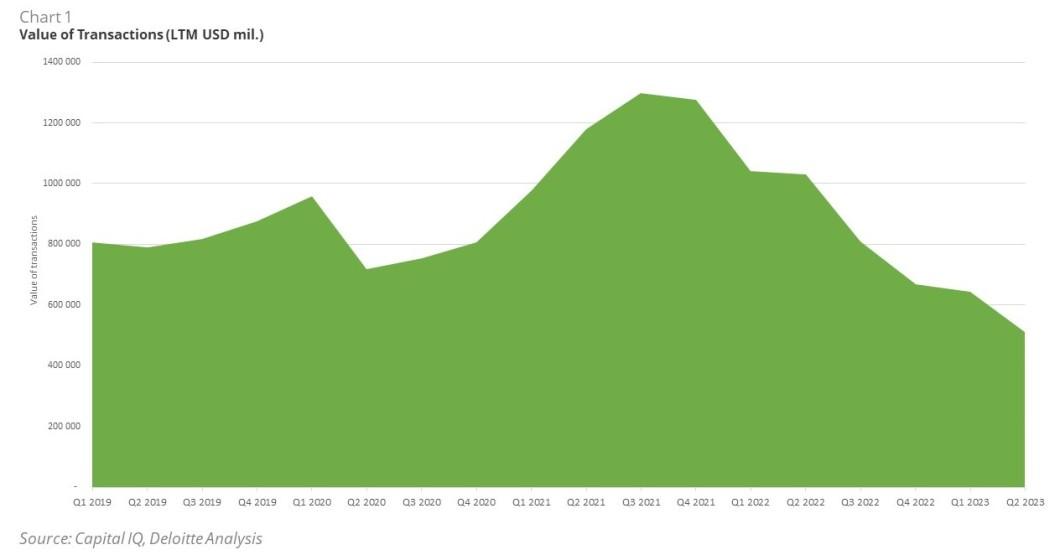

Based on the data published by Capital IQ, the number of deals in 2Q 2023 fell to 2,917 from a total of 3,237 (recorded in the first quarter of this year). This represents a decline in activity of approximately 9.9%. In addition, total deal value, measured as the sum of the value of deals completed in the last twelve months (LTM), also declined from the original US$645 billion to US$511 billion. This decline continues to reflect overall economic uncertainty, lower profits at the corporate level and higher costs of raising capital.

The M&A Index projected a decline to 2,805 transactions for Q2 2023 (a difference of only about 3.8% from actual results). The results are therefore comfortably within the predicted range.

"Despite the economic downturn, there are several potential catalysts that could boost M&A activity in the second half of this year. Well-capitalized companies are actively seeking acquisitions within their core businesses, with sectors such as healthcare, technology and energy showing promising potential."

- Jan Brabec, Partner, Financial Advisory, Deloitte Czech Republic

Although the predicted trend in the number of transactions remains negative for Q3 2023, it must be seen in the context of the overall macroeconomic situation. The rapid decline that characterised 2022 and which also persisted at the beginning of 2023 is beginning to fade and a gradual stabilisation can therefore be expected. This stabilisation is inherently linked to positive economic forecasts and a comprehensive improvement in the macroeconomic situation. Inflation is showing signs of slowing down and interest rates appear to have peaked. The debt ceiling crisis in the US has been averted, bringing relief to the financial markets. The idea that the inflation crisis can be resolved in a soft-landing mode (i.e. without tipping the market into recession) is becoming more and more realistic. This positive development is contributing to increased confidence among investors and strategic players, especially as regards the expansion of their M&A activities. The markets therefore remain capable of a rapid recovery.

The general increase in investor confidence is therefore mainly attributable to a number of factors which implicitly reinforce the ability of the market to recover quickly. Publicly traded companies and private equity funds continue to hold substantial reserves of unused capital (dry powder). Moreover, the volatility of corporate valuations is gradually diminishing, especially when compared to previous downturns, which is generating optimism among investors and strategic players. Despite the strong resistance, there continues to be strong interest from strategic and financial investors in M&A involving significant targets in Europe. These factors greatly enhance the ability of the market to recover quickly, and it remains likely that investors will continue to seek investments in companies with a significant market position, strong financial performance and a viable business strategy.

"Looking ahead, there are several factors that suggest a possible improvement in the M&A market. Inflationary pressures are slowing and there are signs that interest rates have peaked. In addition, the buzz around disruptive technological innovations such as generative artificial intelligence is fuelling optimism."

- Miroslav Linhart, Managing Partner, Financial Advisory, Deloitte Czech Republic

In the current volatile market, active portfolio management remains key to improving corporate strategies and optimising business models. Strategic acquisitions, partnerships and, above all, divestments and carve-outs remain an essential part of risk management. Investors must continue to carefully evaluate their corporate portfolios and consider divesting non-core assets as part of ongoing transformation strategies. Such steps allow organizations to adapt and thrive in an ever-changing environment. It will thus be these transactions - not the giant-sized deals that have continued to decline since peaking in 2021 - that will dominate the M&A market. Therefore, in the coming periods, we can primarily expect an increase in transactions in the mid- and small-cap market driven by the active implementation of strategic growth programmes. These transactions will form a solid basis for future positive market developments.

This type of transactions will be mainly driven by factors that can mitigate the general risks inherent in market realities and create new investment opportunities. These are mainly:

- Well-capitalised companies are likely to seek acquisitions within their core businesses. Sectors that could see increased activity include, in particular, healthcare, technology and energy (particularly in the context of the energy transition).

- M&A activity continues to be boosted by cash balances; at the end of 2022, unallocated private equity ("dry powder") balances were approximately $1.96 trillion. Financial sponsors, currently holding record amounts of capital, are expected to use these funds to make strategic acquisitions.

- Cross-border mergers and acquisitions are expected to return, suggesting an increased number of transactions between companies from different countries. In 2022, the global economy faced many challenges, such as a pandemic, trade tensions between the US and China, and divergent economic conditions in different regions. As a result, cross-border deal making was significantly impacted and saw a decline. However, a recovery can be expected as the impact of these obstacles gradually fades.

- There is an increasing focus on environmental, social and governance (ESG) factors, which are increasingly important for investors and consumers. As a result, companies are expected to incorporate ESG considerations more strongly into their M&A decision-making processes.

ABOUT M&A INDEX

Deloitte M&A index is a forward-looking indicator that forecasts future M&A deal volumes – the number of announced transactions over the observed period – and identifies the key factors influencing the dealmaking conditions on the European Market (characterized as 27 countries of the EU + the United Kingdom). Compiling data from various global databases, including Capital IQ, Mergermarket, Pitchbook, Eurostat, and many more, the model utilizes a combination of statistical and algorithmic tools to provide a comprehensive review of the M&A market activity. The Index is created from a composite of market indicators – specifically pertaining to macroeconomic reality, liquidity, and general market dynamics. These variables are then tested for statistical and economic significance to M&A market volumes. The result is a dynamic, evolving, and up-to-date model allowing Deloitte professionals to accurately access and analyze factors influencing M&A market activity, as well as predict – with a high degree of certainty – the market activity in subsequent periods. The model ¬– in its Beta version – retains high accuracy and is able to predict M&A market activity (in terms of number of announced transactions) with a mean absolute percentage error (MAPE) of around 6,89%.

Related articles

Generali acquires controlling stake in Conning

11 July 2023

FIS sells majority stake in Worldpay

11 July 2023

Nasdaq to buy financial software firm Adenza

12 June 2023