Offensive or Defensive M&A? Build a Framework for Each

19 October 2022

19 October 2022

After a record number of deals last year, companies in many sectors face rapidly changing market and economic conditions that will influence M&A going forward

Mergers and acquisitions (M&A) broke new ground in 2021, by many measures. Against a backdrop of highly challenging conditions, corporates and private equity firms spent some $5 trillion on M&A globally, the highest activity ever recorded and easily surpassing the previous high of $3.66 trillion in 2015.1 In terms of volume, a record 62,600 deals were announced in 2021, up 25% from the prior year, with activity spread across small-, mid-, and large-cap segments. There’s more. Around 144 megadeals (those valued at more than $5 billion) were announced last year, a 65% rise over the previous year and a sure sign of confidence. And in stark contrast to the 2008 downturn—when private equity firms made a dramatic retreat from the markets and deal flows dropped by 65% to $253 billion —private equity was one of the driving forces in M&A this time, spending a record $1.7 trillion on buyouts, culminating in a growth of 124% over the previous year.

Now, more than halfway through 2022, it’s a much different market. Although the pace of dealmaking started the year confidently, progress has been overtaken by factors that just didn’t exist or were less significant a few months ago, including rising interest rates, inflation, and the ongoing Russia-Ukraine war.

The rise of these macroeconomic factors is one good reason for CFOs to consider adjusting M&A strategy for the year ahead, accounting for shifts in risk and opportunity scenarios that frame the severity of how specific markets and companies are potentially impacted. The other has to do with more individualistic competitive factors such as a company’s own operating model agility, strategic positioning, capital return horizon, and brand permission that frame an organization’s respective abilities to effectively respond.

Just how those characteristics can feed M&A strategy was brought into relief during the COVID-19 pandemic. The pandemic affected each industry, sector, and region differently, and the respective recovery cycles for each progressed at different rates, meaning the range of response options was likely to be asymmetrical and more complex than in prior market contagions. For example, in sectors that were disadvantaged by pandemic conditions such as aviation, automotive, retail, and hospitality & leisure, some made significant defensive M&A moves to salvage value and stay afloat, while many made consolidation moves to safeguard their market positions. Other sectors, including health, shipping, technology, and telecoms, experienced a boost in demand during the pandemic and were able to move on more offensive M&A transactions to boost revenues and capture new markets. Another range of asymmetric responses we saw accelerate during the pandemic was the rise in alternative M&A deal types, such as alliances, partnerships, ecosystems, and platforms, rather than the often larger scale traditional asset swap transactions. Today, one of the biggest challenges unfolding for many companies is the steep rise in commodity prices linked to Russia and Ukraine, as well as other inflationary pressures, all of which are adding strains to already stretched supply chains. Central bankers have indicated they will continue to use rapid interest rate hikes to contain inflation, which should leave companies looking for ways to recalibrate their debt strategies to reflect changing market conditions and prepare for rising interest rates and possible lender limitations on cyclical businesses. There remain substantial levels of liquidity in the debt markets that should support a strong lending appetite for highly defensive assets. At the same time, lenders will set a high bar on diligence for assets exposed to economic cyclicality, commodity prices, supply chain disruptions, and inflationary pressures. As part of a strategy reset, CFOs should also anticipate greater public scrutiny of corporate environmental, social, and governance (ESG) responsibilities and investor expectations, to deliver profits with purpose. For example, fund managers representing a total of $121 trillion of assets under management have signed the UN Principles for Responsible Investment, and they are increasingly holding companies accountable for performance on ESG parameters. Many limited partner investors are also putting pressure on private equity and venture capital firms, and this has led to the launch of the ESG Data Convergence Project to advance more standardized reporting. Similarly, a Deloitte survey shows 60% of CFOs at listed companies believe their overall performance on ESG issues has a high or moderate impact on their cost of capital.

To help make sense of the many factors at play, consider a look at the beneficial tailwinds that will likely support M&A markets in the year ahead.

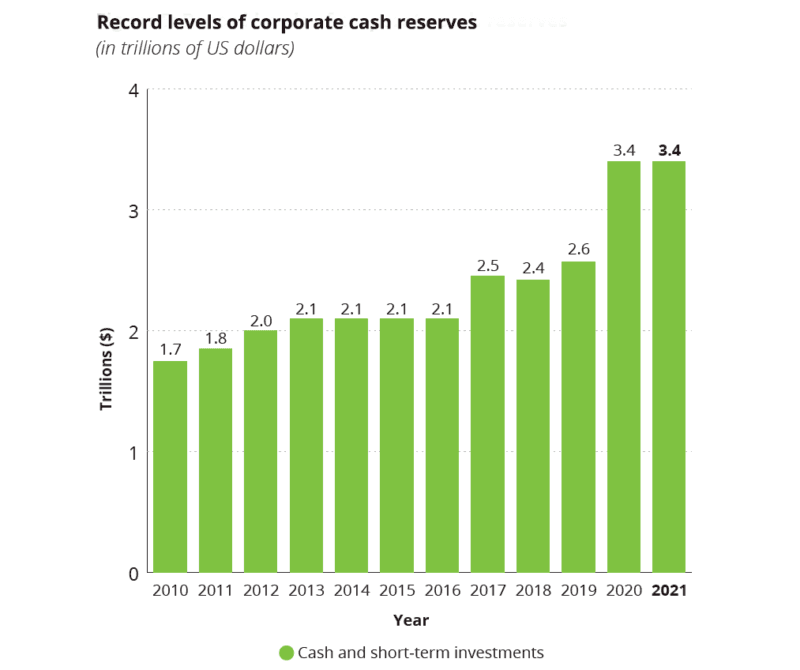

Record cash reserves. Since the start of the pandemic, companies have taken decisive measures to bolster their cash piles, now amounting to a record $3.5 trillion —a very substantial arsenal. Dealmakers would be wise to heed the lessons of the 2008 financial crisis, when a compulsive cash accumulation culture emerged in the aftermath that inhibited the evolution of potential future-shaping investments and deals. A Deloitte study, “The Cash Paradox,” found that markets rewarded companies that invest excess cash in the pursuit of growth. The analysis found that since 2000, such companies managed to increase their share price by 632%, nearly twice the growth rate experienced by their cash-hoarding counterparts.

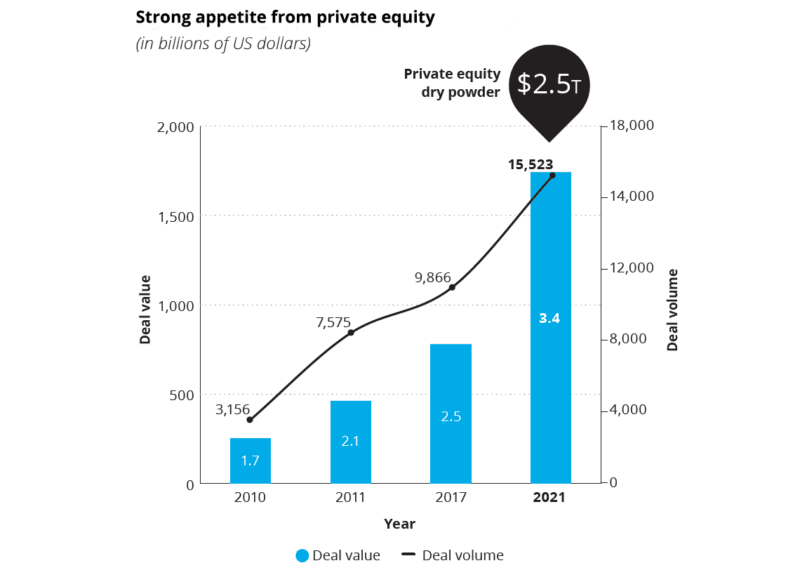

Private capital. As of 2021, private equity firms have been sitting on an estimated $2.5 trillion of “dry powder”8 and they’re likely to continue to be active in M&A markets. Increasingly, they are looking beyond financial reengineering to favor technology platform plays, digital transformation opportunities, and investments aligned with macro themes, such as ESG.

Meanwhile, private equity is stepping up investment in the growth capital segment, competing with traditional venture capital funds, which invested a record-breaking $621 billion in disruptive startups in 2021, and is expanding into emerging markets, such as Africa. Pension funds, family offices, and sovereign wealth are also making their mark on M&A. Historically, they placed their vast resources in wealth and private equity funds; however, a growing number of these investments are being handled directly in-house.

Cross-border trade lanes. In 2021, cross-border M&A also reached record levels. The North America-Europe M&A corridor was the busiest, with $545 billion worth of deals. In addition, North American investment into the Asia Pacific region grew by triple digits to reach $191 billion. This trend is likely to continue. In fact, a recent Deloitte snap poll shows that 68% of U.S. companies are considering international markets for new growth opportunities.

Meanwhile, the following are challenging headwinds that most companies will need to reckon with.

Rising inflation and interest rates. The sharp revival of inflation has started to put pressure on consumer spending. At the same time, the U.S. Treasury yield curve has started to flatten, which suggests investors are expecting an economic slowdown.12 Such conditions put pressure on corporate profits, bonds, and stock prices. That could prompt companies to review cash flow forecasts and recalibrate financial strategies to factor in inflationary pressures and expectations of interest rate hikes in their business models. Some companies might consider divesting non-core assets to free up working capital. Others might opportunistically acquire competitors to buffer against rising input costs through procurement synergies, digitization efficiencies, and boosted pricing power.

Interestingly, a Deloitte analysis of nearly 40 years of historical U.S. M&A, inflation, and Federal Reserve interest rate data shows only moderate correlation between M&A and those macroeconomic indicators. In fact, between 1995 and 1999, as well as in 2007, an upward M&A cycle was undeterred by both rising inflation and hawkish rate setting. There also was strong historical evidence that M&A markets tend to recover quickly from crisis conditions once uncertainty subsides.

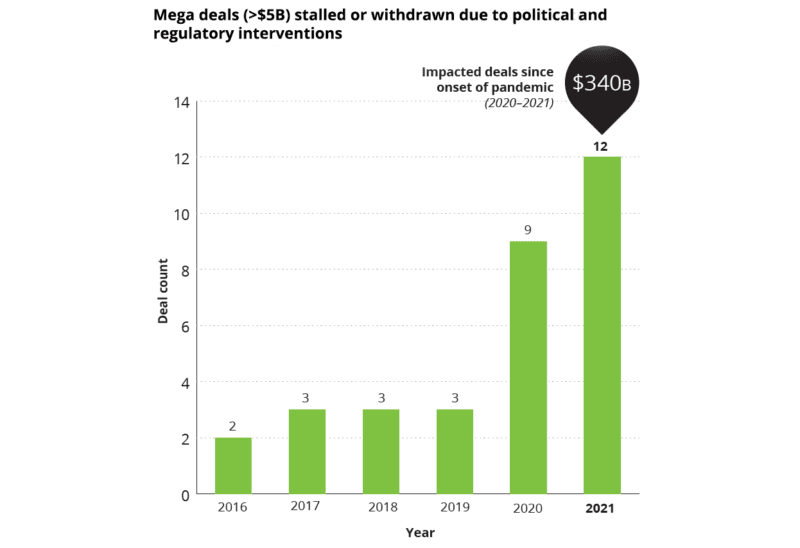

Regulatory hurdles. Elevated levels of M&A activity are catching regulators’ attention, and amid severe scrutiny, some $340 billion worth of deals have been impacted since the onset of the pandemic. There is also constant pressure on deals from activist funds, shareholders, and even consumers, creating further uncertainties.

Companies will need to demonstrate the long-term benefits of their deals to regulators and broader stakeholders against a backdrop of protectionist instincts that are clouding M&A. Crucially, whenever a deal is thwarted, investors will expect a “Plan B” strategy to be initiated promptly. Deloitte analysis shows that within one year of a proposed transaction’s withdrawal, about half of acquirers and targets remained active in the market and completed new deals.

Rising valuations. In 2021, the average price-to-earnings deal multiple rose sharply to 26.5, the highest since 2015.15 Pandemic conditions gave a boost to valuations in many sectors, such as home fitness and media streaming companies. But due to changing conditions and consumer habits, recent financials might not be accurate predictors of future performance. When evaluating opportunities, companies should undertake rigorous valuation that is supported by dynamic modeling, scenario planning, and detailed value-extraction plans. That should help strike a balance between mature acquisitions targeting focused returns and those based on the promise of exponential disruptive growth.

The bottom line: To succeed in an emerging post-pandemic world, corporate leaders must learn to calibrate their M&A strategies to a rapidly transforming environment.

Click here to read the full report, “Charting new horizons, M&A and the path to thrive.”

Offensive or Defensive M&A? Build a Framework for Each

19 October 2022

HARDWARIO has successfully entered the START market

18 October 2022

Launch of NORTONLIFELOCK emissions trading

14 October 2022

Porsche IPO

14 October 2022

Komerční banka - online IPO instruction

12 October 2022

2023 financial services industry outlooks

12 October 2022

Adobe acquisition of Figma

10 October 2022

Subscription of HARDWARIO shares has been launched

4 October 2022