Euronext in talks to buy Allfunds

23 February 2023

15 March 2023

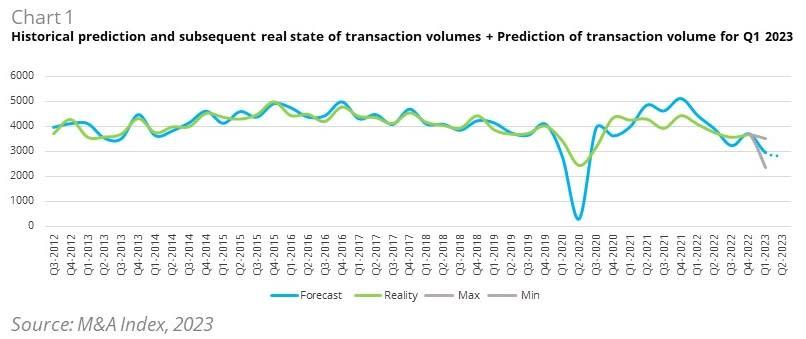

In the first quarter of 2023, macroeconomic challenges such as inflation, rapid monetary tightening and a less than optimistic economic outlook will lead to a significant decline in M&A activity. The index forecasts 2,940 announced deals for the first quarter of this year. In the fourth quarter of 2022, the total was 3,680 deals, so the model predicts a decline of more than 20%. Total deal value (measured as the sum of the value of deals done in the last twelve months) also declined, from $809.9 billion to $677.4 billion.

The current development on the market portrays the inherently adverse relationship between uncertainty and the M&A markets. In this context, the market activity – in terms of both values and volumes – can be characterized as a function of economic certainty, interest rates, and general macroeconomic environment. In this context, despite the sharp drop in transactions, the market activity still carries the potential for a speedy recovery, with health of the banking system, strong cash balances, and continued expansion in cross-border deals working to offset the severe headwinds on the market.

"Despite the sharp decline in transactions, market activity may be supported by high cash balances of private equity investors. Private equity funds held approximately USD 1.96 trillion at year-end. These entities continue to seek investments in quality assets such as firms with strong market positions, long history and workable business strategies. In addition, the rising cost of capital is constraining market activity and creating downward pressure on valuations. This consequent correction in market multiples brings new consolidation opportunities, especially for strategic investors," explains Jan Brabec, partner in Deloitte's Financial Advisory Department.

Among other things, local markets are also expected to continue to support cross-border transactions (particularly in the North America-Europe corridor), which form a key part of the European M&A market. In 2022, investments by North American entities accounted for transactions worth a total of USD 211 billion, approximately 27% of the total value of transactions in Europe. According to a Deloitte survey, more than 68% of US companies consider international expansion as a necessary part of their continued growth. These countervailing influences can significantly boost market activity and remain a necessary variable for further market development.

"Macroeconomic conditions and market volatility have always been key factors driving M&A activity. In an environment characterized by high inflation, high interest rates and a slowing global economy, deal making is more challenging due to increased uncertainty, higher funding costs and a more cautious investment climate. However, unlike the 2008 financial crisis, there is ample equity capital available to support strategic and financial investors. Also, banks, while cautious, remain in good shape and are ready to finance leveraged transactions,"adds Miroslav Linhart, senior partner in Deloitte's Financial Advisory Department.

M&A Market Summary 2022

Uncertainty continued to prevail in global markets throughout 2022. The war in Ukraine, the looming recession, and the COVID-19 pandemic (in the form of disrupted supply chains) had a major impact. The S&P 500 Index posted its worst annual performance in 14 years in 2022, declining nearly 20%. In Europe, the situation was not much different and the STOXX index closed at 424.89 on 31 December, down 12.4% for the year. Similarly, the M&A market saw a significant drop in the number of deals, from 16,942 in 2021 to 15,249 in 2022, a decline of 10%. The same applies to the total value of transactions, which decreased by 46.9% year-on-year.

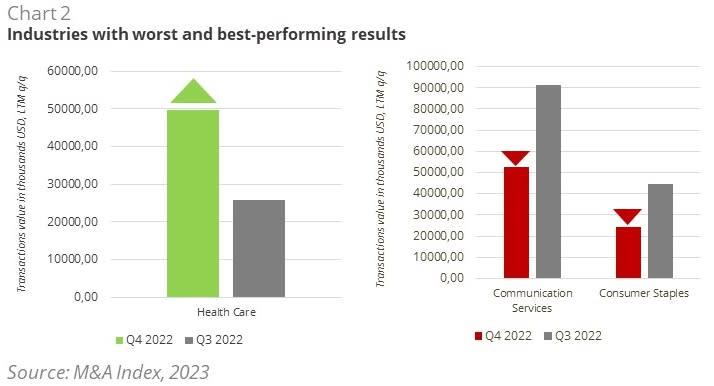

From an industry perspective, the healthcare sector was the only one to see an increase in total transaction value in Q4 2022, up 93%. In contrast, all other sectors saw a decline. The biggest declines were in the consumer goods (-46%) and communication services (-42%) sectors.

The European M&A market has suffered a significant downturn as a result of the economic turmoil. With the exception of the mature markets (France, Belgium and Sweden) and the more dynamic emerging markets (Slovenia, Croatia and Romania), all markets in this area have seen a rapid decline in the number of deals. Overall, the Balkans have shown greater resilience to macroeconomic pressures. The most affected regions were Luxembourg (-30.7% y/y), Spain (-35.5% y/y) and the Czech Republic (-45.5% y/y).

What is the Deloitte M&A Index

The Deloitte M&A Index is a forward-looking indicator that forecasts future M&A market volumes - the number of announced deals over a reporting period - and identifies the key factors influencing deal-making conditions in the European market (characterised as the EU27 + UK). The model compiles data from various global databases, including Capital IQ, Mergermarket, Pitchbook, Eurostat and many others, and uses a combination of statistical and algorithmic tools. The index consists of market indicators - specifically relating to macroeconomic realities, liquidity and general market dynamics. Despite the increased volatility of recent periods - caused primarily by the exogenous effects of the Covid-19 pandemic and the war in Ukraine - the model retains statistical and econometric significance.

Deloitte M&A Index 2023

The number of European transactions will fall by 20 percent in the first quarter of 2023.

Euronext in talks to buy Allfunds

23 February 2023

What next after the cryptocurrency euphoria slump?

3 February 2023

Central Europe Private Equity Confidence Survey

2 February 2023

Czech fintech Orka Ventures continues to grow

25 January 2023

2023 financial services industry outlooks

12 October 2022

European CFO Survey – Spring 2022

9 August 2022

2022 financial services industry outlooks

9 August 2022