You cannot devote only thirty minutes a day to trading

16 October 2021

6 January 2022

Companies established for the sole purpose of public trading on the stock market are becoming ever more popular. Although in recent years these “blank check companies” have been popular mainly among American investors, they are now also enjoying more attention in Europe, where more than thirty SPACs have been established since the beginning of 2021. We have summarised the utility of SPACs, the way they operate and their importance during the coronavirus crisis in our article.

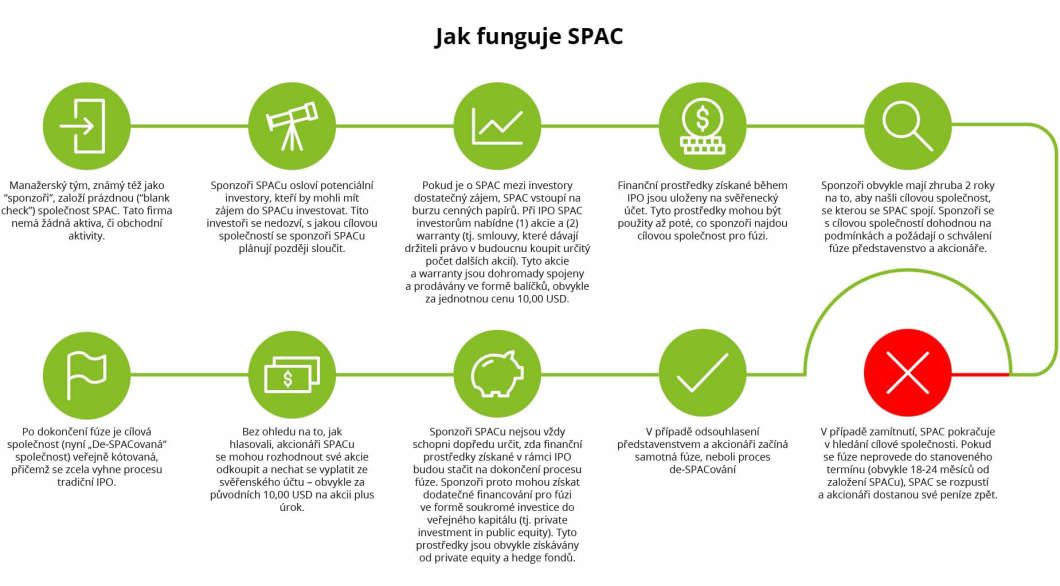

The term Special Purpose Acquisition Company (SPAC) essentially refers to a company that has no business activities, no assets and usually no offices or employees. The sole intent of establishing such companies is to carry out an Initial Public Offering (IPO), raise funds, and merge with another existing company.

Investors in a SPAC during the IPO process usually do not know which company will be invested in later on by the SPAC; the future of such a trade is based on the expertise of SPAC founders and their ability to identify and close a profitable deal. It is no wonder then that among the founders of successful SPAC projects are mainly well-known investors, such as Gary Cohn, former COO of Goldman Sachs, or Bob Diamond, a former CEO of Barclays. In recent years, however, sports celebrities have also joined the list of SPAC founders – the tennis player Serena Williams and basketball player Shaquille O’Neal among others.

SPAC as the symbol of the 21st century

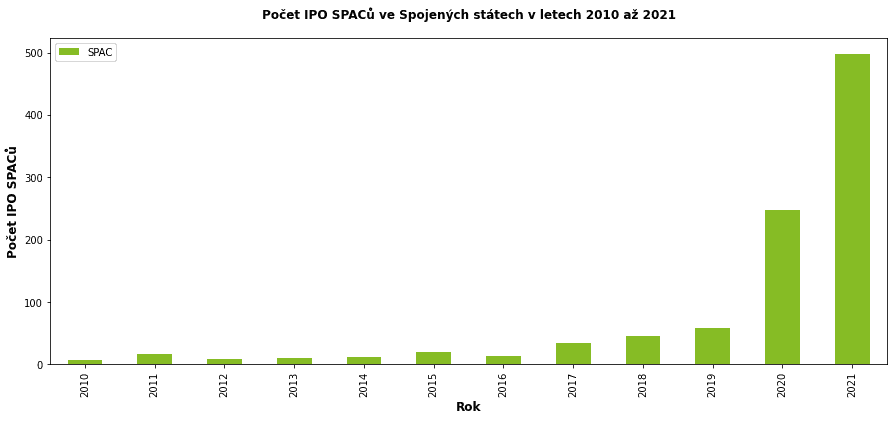

Special purpose acquisition companies were first created in the 1990s, but they have gained popularity among investors only recently. For example, in the US in 2010, there were 7 IPOs (out of 160 in total) realised through SPACs on the US Stock Exchange. In comparison to 2020, SPACs were involved in more than half of all American IPOs; 248 out of 450 IPOs were arranged through SPACs, to be exact.

In 2021, SPACs gained a foothold in Europe, with more than 30 special purpose acquisition companies listed since the beginning of the year. Euronext Amsterdam leads the way with more than 40% of European SPAC listings along with three on the Frankfurt Stock Exchange. The London Stock Exchange saw its first SPAC listing (Hambro Perks Acquisition Co.) in November 2021. It took place shortly after the British government facilitated the access of SPACs to financing.

SPACs in the Czech Republic

The first SPAC listing is also underway in the Czech Republic with the involvement of WOOD & Company led by Vladimír Jaroš. Mr Jaroš says, “The listing of this SPAC brings a new form of entering the stock exchange to Czech companies. This approach is faster than a typical IPO and requires a merger with a SPAC. We want to show that the capital market here works and that we, with our supra-regional reach, can link good business ideas with people who are willing to invest, risk and make money in the stock market. One of the ways to do that faster in a new way is choosing the SPAC route. It is not our original idea – such companies have existed for several years in western markets.”

The current situation and future development of SPACs

Despite SPACs’ growing popularity, some scholars and experts in corporate finance are sceptical of them. For example, Usha Rodrigues, the Professor of Corporate Finance at the University of Georgia, compares SPAC to a “hasty marriage in Vegas”. The flood of new SPAC projects brought many private companies to American stock markets. These private companies sidestepped the route of a traditional IPO which requires months of planning and preparation. The SPAC process does not require strict due diligence, among other things, which makes the fusion process simpler and faster. At the same time, Rodrigues says that a lower level of due diligence may lead to an inaccurate company valuation and later litigations. Bloomberg studied the financial results of SPAC projects using an empirical method. They analysed more than 190 SPAC mergers which launched private companies onto public markets since 2019. Their findings show that special purpose acquisition companies tend to underperform public companies that had gone through a traditional IPO. American SPACs that had gone through a merger have grown by 11% on average since their IPO. In contrast, companies that had gone through a traditional IPO have grown by an average of 61% since going public. In addition, an index of 25 companies that have gone public after merging with a SPAC has so far had lower return than S&P 500 ¬¬– by more than 50 percentage points. These statistics show that while some projects do well after merging, it is not the case for most of them.

The impact of the coronavirus crisis on SPAC popularity

During the current coronavirus pandemic, financing in the form of a SPAC is more attractive than ever before for some private investors. Due to the high market volatility, it is, for instance, complicated to properly time a traditional IPO. The price of a company’s stock can drop significantly just because the market dips on the day of entering the market. If the company is also conservative and offers too low prices, it risks undervaluation. In contrast, the SPAC route lowers the uncertainty. In comparison to a traditional IPO, the target company can negotiate its stock price as part of the investment agreement. In other words, the target companies may lock in the price and thus protect themselves from uncertainty on the IPO market. Another benefit for the selling company besides the price is the faster completion of the merger through a SPAC in comparison to a typical IPO. The merger of a target company with a SPAC can be completed in as little as three to four months; in comparison, preparing a traditional IPO takes between 12 and 24 months on average. SPAC financing is particularly beneficial for small- and mid-sized companies that are in the early stages of business but want to continue financing their development, invest in brand awareness or carry out acquisitions. These types of companies often do not qualify for a traditional IPO. However, by merging with a SPAC, they can access the liquidity they need while cooperating with experienced investors who often partake in SPACs.